The Year(s) Ahead in Media - Concentration

The Role of Networks in Concentrating Power and Attention

Note: This is the third post in a four-part series that discusses four tectonic trends (fragmentation, disintermediation, concentration and virtualization) that will determine the flow of value along the media value chain in coming years. Here are part 1 and part 2.

Tl;dr:

The first two trends, fragmentation and disintermediation, result from technology systematically lowering the barriers to produce, market, distribute and monetize content.

This trend, concentration, is the consequence of putting everyone on a big network. Networks are subject to powerful positive feedback loops that produce extreme outcomes. In the case of media, they concentrate both power (on the supply side) and attention (on the demand side).

Historically, distribution of media was siloed, local and one-way. Today, most media is distributed on universal, global, two-way networks.

The positive feedback loops on networks produce network effects and information and reputational cascades.

Network effects are a supply-side effect, because they influence market structures. They produce winner-take-all (or most) markets, concentrating power and value in a few companies.

Combined with these companies’ global reach and universality, that means traditional media companies are now contending with distributors and competitors with unparalleled scale, resources and the ability to cross-subsidize losses indefinitely. Creators and consumers are contending with “new gatekeepers” with unprecedented power, although they wield it differently than traditional intermediaries.

Cascades are a demand-side effect, because they influence the distribution of consumption.

Hits are self-perpetuating—the rich get richer—because people interpret popularity as a signal of quality (information cascade) and/or social currency (reputational cascade). This results in power law-like popularity distributions: a small number of outsized hits (in the “head”) and a vast number of misses (in the “tail”).

These extreme popularity distributions shift bargaining power to the rare breakout talent, hollow out the “middle” of the curve and increase the risk of making content.

The fourth and final post discusses the last trend, virtualization, and ties it all together.

3. Concentration: The Role of Networks

Prior to the Internet, the distribution of media was local, siloed and one-way. Media products were delivered through local, format-specific outlets (movie theaters, retailers, local TV and radio stations, local newspapers) and consumers had no feedback mechanism, other than voting with their pocketbooks or attention.

Today, most media is consumed on global, universal, two-way information networks.1 That includes social networks (YouTube, TikTok, Instagram, Facebook, Snapchat), of course, but any site or app that has a return path (whether an active return path, such as the ability for consumers to like, comment or share, or a passive return path through data collection) is a network. Netflix, Amazon, Spotify, cable systems, Apple News, The New York Times’ website, this Substack, are all networks.

Let’s unpack global, universal, two-way.

The reach of these networks is “global” because they aren’t bound by geography (although they are sometimes constrained by the rights they own or local regulations).

They are “universal,” in the same sense I used the word in part 1: since all media goods have been reduced to bits, these networks can distribute any kind of media. (Apple and Amazon, for instance, distribute newspapers, magazines, books, software, games, TV shows, films and music.)

Most important is the term “two-way.” On networks, the behavior of every node can effect every other node, which results in powerful positive (also called “reinforcing”) feedback loops2.

For media, the growing prevalence of networks, and particularly the positive feedback loops on networks, has two important implications, one supply side and one demand side:

One type of positive feedback loop is network effects, which lead to winner-take-all (or most) outcomes, concentrating power and value in a few networks. Combined with these networks’ global reach and universality, that means traditional media companies are now contending with distributors or competitors with unparalleled scale, resources and the ability to cross-subsidize losses indefinitely. Creators and consumers are grappling with new gatekeepers.

Another type of positive feedback loop is cascades that concentrate attention. On networks, hits are self-perpetuating because people interpret popularity as a signal of quality (information cascade) and/or social currency (reputational cascade). This results in power-law-like popularity distributions: a small number of outsized hits (in the “head”) and a vast number of misses (in the “tail”). These extreme distributions counteract the fragmentation I discussed in part 1, but they also shift bargaining power to the talent in the head, hollow out the middle and increase the risk of making content.

Let’s dig into both.

Network Effects in Media

So much has been written about network effects that I will try to only hit the high points.

Media has always favored the “big;” network effects bring a new kind of “big.”

Media has long been characterized by supply-side economies of scale, namely the benefits of being big. To take a few examples from my alma mater, Time Warner: Warner Bros. had the largest global distribution footprint of any studio, so any film it distributed had a better chance of succeeding, enabling it to attract the best projects. HBO had the most subscribers of any premium pay TV network and generated the highest wholesale price, so it could spread content costs across the largest revenue base. CNN has the largest global newsgathering infrastructure, best positioning it to cover breaking news anywhere in the world.

By contrast, network effects are also called demand-side economies of scale3, meaning that users benefit directly as the network grows. The canonical example is the telephone. The first telephone was worth nothing, because, as the only phone on the network, it could neither receive nor send calls. Each phone that subsequently joined the network increased the number of other people who could send or receive calls and therefore increased the value of the network to all users.

Network effects can vary in strength, based on a few factors, such as the value derived from the network effect (relative to the total value of the service) and the switching costs or ease of multi-homing (using more than one service). Companies that operate multi-sided markets that facilitate interactions between 3rd parties and consumers, often called platforms, tend to exhibit very strong network effects. The more participants on each side of the market, the harder it is to coordinate a move to an alternative platform. Operating systems (Windows, iOS, Android); peer-to-peer sharing economy networks (AirBNB); used goods marketplaces (Ebay); and social networks are all examples.

Winner Take All (or Most)

The advent of media consumption on networks has brought network effects to media, to varying degrees. For instance, people consume a lot of media on Facebook, which has extremely strong network effects because it’s pretty much impossible to move your whole social graph somewhere else. YouTube has relatively low switching and multi-homing costs—you can easily search for video somewhere else—but it exhibits very strong network effects because of the sheer scale of creators, advertisers and consumers on the network (no one has an incentive to go anywhere else). Netflix has network effects because the more users, the more consumption data it gathers and the better its recommendation systems. Similarly, for Spotify, the more users, the more playlists to follow. But, in comparison to Facebook or YouTube, Netflix and Spotify have relatively weak network effects, because the quality of a recommendation system or access to other people’s playlists are secondary to the quality and breadth of content and other product features.

The platforms with the strongest network effects have developed unprecedented global scale, with unparalleled resources (enormous capital for R&D or acquisitions, top-tier talent and first-party data), and they have an almost unassailable competitive position. In addition, because of both their size and their universality (meaning that they can enter new information verticals with relative ease), they are able to lose vast sums of money when entering adjacent markets, either to establish a competitive beachhead or because they expect these losses to be offset by larger gains in some other part of their businesses. If the latter, they can theoretically lose money in any given adjacent market forever.

The smallest platform, Meta, is as big as the entire global media industry.

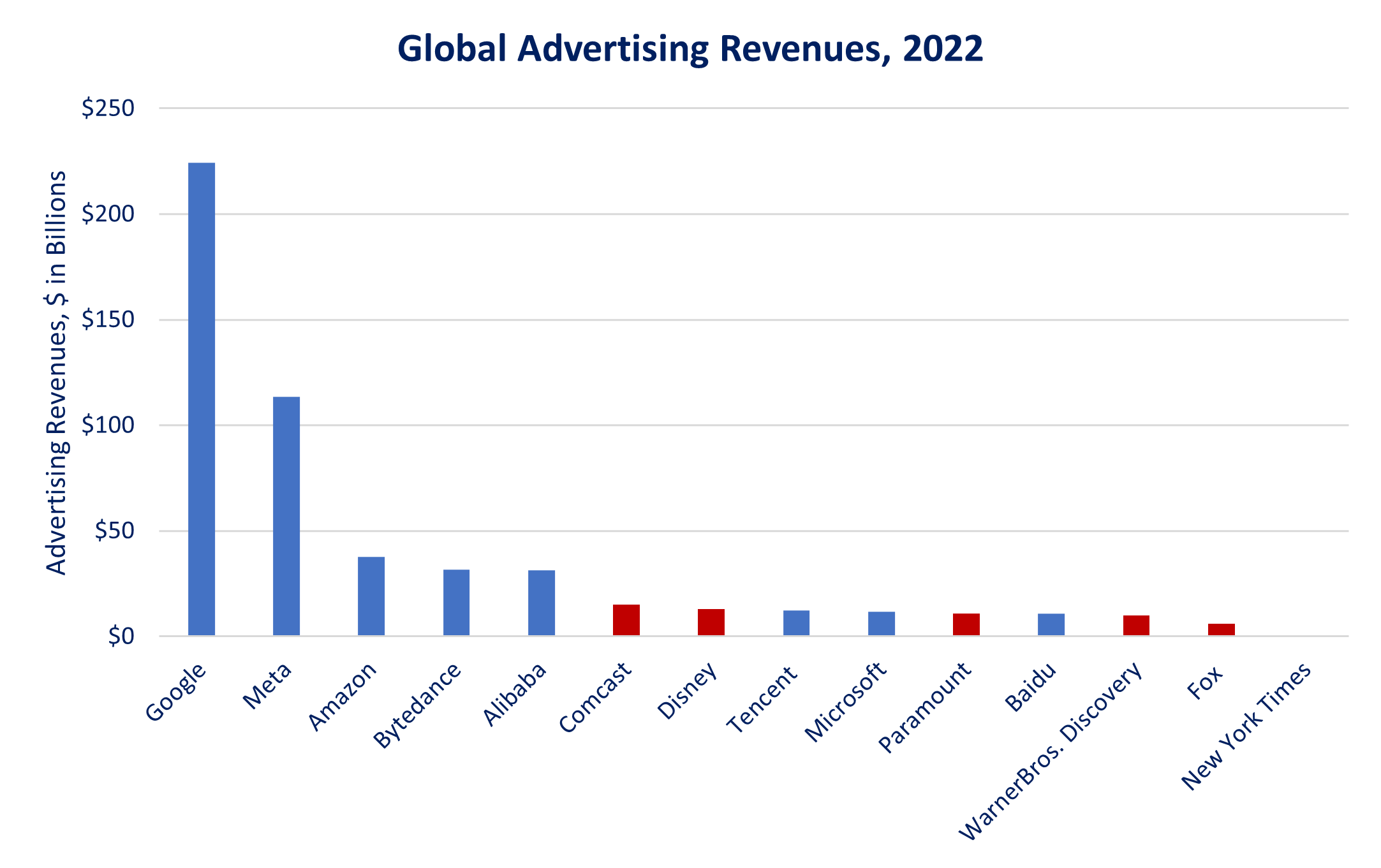

It seems hardly worth re-litigating these points, which have been made elsewhere many times. But here are two charts to hammer it home. Figure 21 shows the market capitalizations of the largest platform and media companies. Figure 22 shows a similar comparison for global advertising revenue in 2022. The media industry is a gnat on the backsides of these behemoths. Note that the smallest of the platforms, Meta, has about the same market cap as the entire global media industry, combined (including every public media company not shown here).

Figure 21: The New Competitive Dynamic in Media

Source: Yahoo Finance.

Figure 22: The New Competitive Dynamic in Media (Redux)

Notes: Disney and Fox are fiscal years, ended September and June, respectively.

Source: Company reports, Statista, Author estimates.

Meet the New Boss, Not the Same as the Old Boss

Having established what has already been established many times, let’s get to the “so what?” The media industry has always had gatekeepers, or what I referred to above as “traditional intermediaries.” Are we just replacing old gatekeepers with new gatekeepers? In some ways yes, but there are important distinctions between them.

The new gatekeepers don’t mind the gates

Disney, Warner Music and Take-Two are gatekeepers in the sense that they completely control what films, albums or games they make or distribute. For an actor or director to “make it” in Hollywood, for instance, means that she has to convince a major studio to make a bet on her. YouTube, Spotify and Steam do not exercise nearly as much control. While they may change terms of service, retain ironclad control and ownership of data on their platforms, extract hefty taxes and sometimes “de-platform” or “de-monetize” creators for seemingly capricious reasons, anyone can upload content to these platforms permissionlessly (subject to terms of service).

Also, while the “new gatekeepers” may curate the content on their platforms, for the most part they do so through recommendation algorithms that largely depend on user behavior, not on a development executive’s judgment or the platforms’ corporate interests (even if they sometime put their thumbs on the scale). This difference in degree of oversight has both a societal benefit and cost. The former is much, much lower barriers to creation and, therefore, much greater diversity of viewpoint and artistic breadth; the latter is lack of oversight over potentially harmful information.

They take no risk and retain no equity

One of the reasons that the traditional intermediaries exercise such control over the content they produce is that they take substantial financial and reputational risk. They finance production, spend heavily on promotion and their brands are closely associated with the content they make. In exchange for taking on this risk, understandably they retain much of the upside. Film and TV studios, for instance, may provide profit participation to talent, but it is usually small and only after the studios have recouped their costs. Platforms like YouTube, Spotify, Substack or Patreon (usually) take no financial risk and generally have a fixed revenue share or, in the case of sponsored posts on YouTube, TikTok or Instagram, take no share at all. But they also usually do little to promote content beyond what is surfaced by the algorithm (or, in the case of Patreon, nothing at all). For creators, it is sink or swim.

They facilitate direct relationships between creators and consumers

Traditional intermediaries’ marketing efforts are generally focused on a product (a movie, TV show, game, album, etc.) and they will market the talent behind these products only when it benefits the product. (An exception is music, where those or one and the same.) On platforms, the creator is the product and is therefore better able to forge direct relationships with fans.

Can Anything Stop This Concentration of Power? Maybe

At the beginning of this series, I described these four trends as tectonic and “(probably) unstoppable.” Can anything stop these platforms from becoming even more powerful? There are a few possibilities.

Regulation could cramp their styles, but don’t hold your breath. There are a variety of antitrust lawsuits and regulatory efforts that are aimed at preventing anti-competitive and anti-consumer behavior by the largest platforms, including the U.S. vs. Google (with a ruling expected in May) and the recently-passed Digital Markets Act (DMA) in the EU. The U.S. is also reportedly close to filing an antitrust suit against Apple. In the case of the lawsuits, however, the outcome, length of potential appeals and recommended remedies, if any, are all very hard to predict. The U.S. vs Microsoft was arguably the most successful antitrust suit against a technology company (if we don’t include the breakup of AT&T), but more than 20 years later, Microsoft is still the “M” in FAMGA. The DMA provides a framework for rules and consequences for what it deems “gatekeepers.” But it is hard to either litigate or regulate away network effects.

It’s hard to regulate away network effects.

Cryptonetworks promise to break the platforms’ stranglehold. The main ideological underpinning of crypto is that since it is intrinsically decentralized, it will redistribute power and value from centralized institutions to creators and users. The great debate is whether the potential practical benefits of a decentralized Internet will outweigh the inherent inefficiency of decentralization enough to spur widespread adoption. As I wrote in Does Crypto Create Value or Just Redistribute It?, I’m a believer. Time will tell.

The great debate in crypto is whether the potential practical benefits of a decentralized Internet will outweigh its inherent inefficiency.

AI agents could intermediate platforms. The idea of autonomous agents that can understand and fulfill open ended natural language requests has been around for decades (“open the pod bay doors, HAL”) in science fiction. Following the launch of ChatGPT, plug-ins, various co-pilots and customizable GPTs, it’s a lot easier to see how this would work in reality. (Or, see the rabbit r1, an AI mobile device unveiled a few weeks ago.) Imagine that everyone has a personal AI agent that they grant (highly secure, encrypted) access to personal data, like online activity, content consumption, health history, financial information, etc. It could even have access to your wearable for a real-time understanding of your mood or, as Bill Gates suggests, an earbud that hears everything you do. Such an agent could act as a universal media aggregator and suggest content based on your prior preferences and its perception of your need state. For instance, let’s say it pulls up all the social posts that it anticipates you might find interesting, aggregating from X/Twitter, Instagram, Facebook and a potentially unlimited number of decentralized social networks. At that point, you would become indifferent to where something was posted, where you post and where your friends are or aren’t. A lot is unclear how these kinds of agents evolve (do you have one or many? what’s the UI? how do they monetize? are they created and owned by the largest platforms themselves? are platforms able to block or prohibit them?), but in theory they could insert a new layer between consumers and platforms and undermine the platforms’ network effects.

Power Law Popularity Distributions

Why the Internet fragments attention is intuitive. It lowers the barriers to more stuff and more stuff = less attention per unit of stuff. But it also concentrates attention, producing hits. See last year: Taylor Swift, The Mario Bros. Movie, The Legend of Zelda: Tears of the Kingdom, The Golden Bachelor and so on. As mentioned, the reason for this apparent contradiction is that the Internet is a network and networks are subject to positive feedback loops. In other words, people’s content choices are influenced by other people’s content choices.

People’s content choices are influenced by other people’s content choices.

Last year, I wrote a lengthy piece on this topic, called Power Laws in Culture, which proved to be one of my most popular posts. But the main idea is that hits are self-perpetuating because people interpret popularity as a signal for quality and/or social currency. The underlying mechanisms are called information and reputational cascades:

Information cascades. When confronted with so much choice, consumers need filters. One of those filters is popularity, because people assume that other people’s choices contain valuable information (i.e., “the most popular stuff must be popular for a reason, right?”). When many people do this successively, it results in an “information cascade.” This is sometimes called cumulative advantage, preferential attachment or the “rich-get-richer effect,” whereby popular things tend to get more popular and unpopular things stay unpopular.

Reputational cascades. People also conform to the group choice, either subconsciously or because they want to signal their allegiance to the group. This is referred to as a “reputational cascade.”

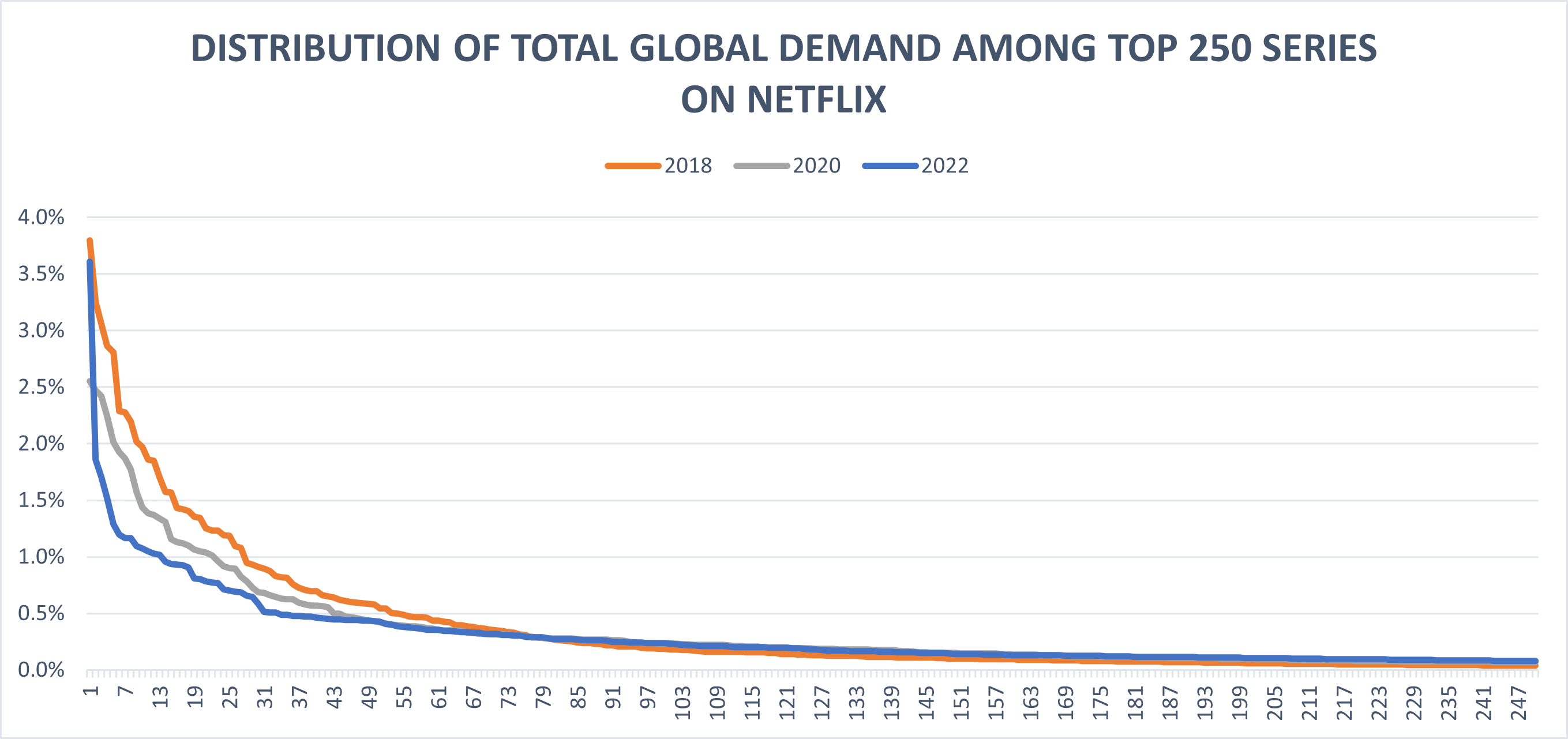

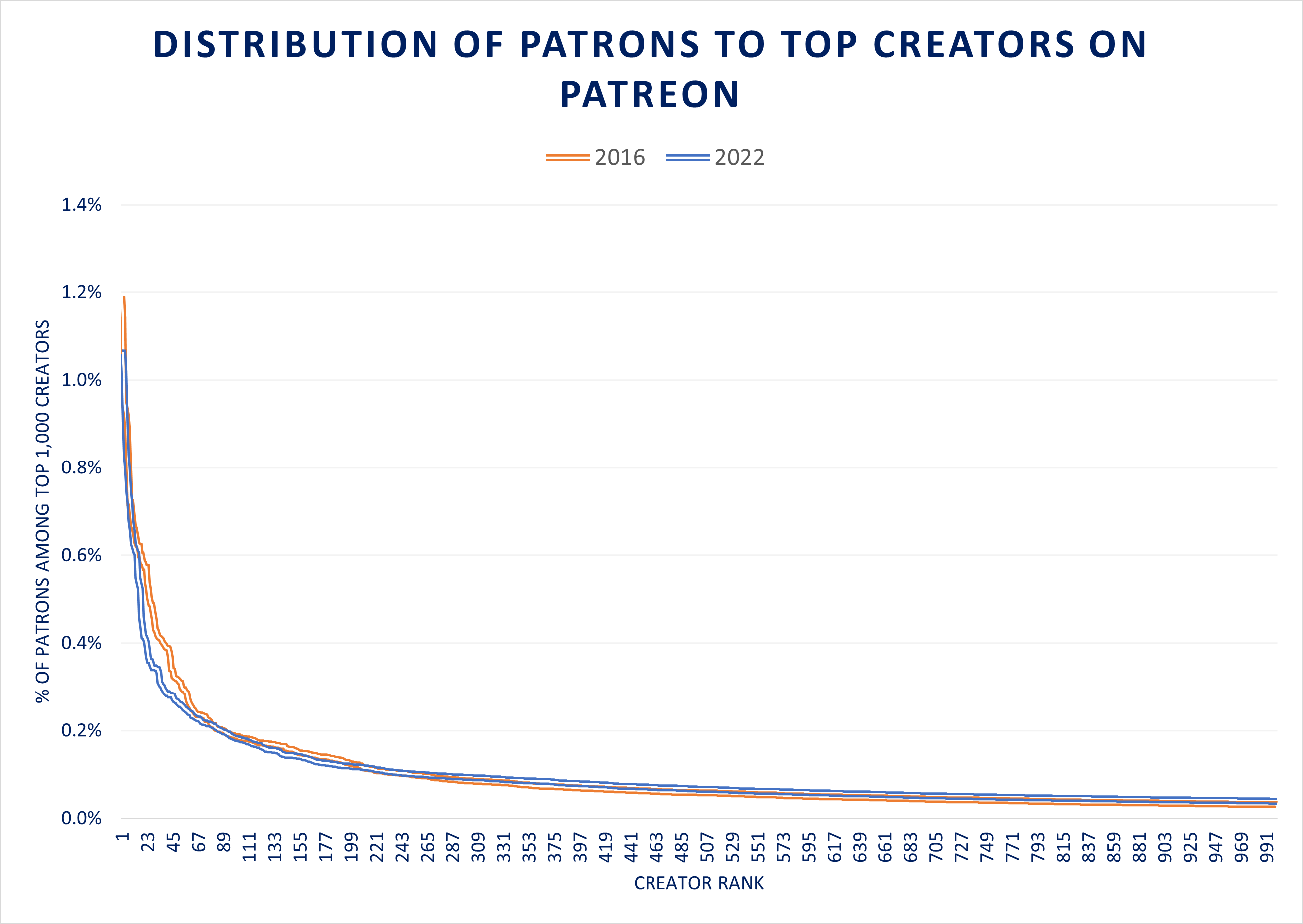

When you combine the Internet’s tendency to simultaneously concentrate and fragment attention, you get power law-like popularity distributions: a very narrow head, with a few hits, and a very (very, very) long tail of obscure misses. In Power Laws in Culture, I showed empirically that there are persistently, and sometimes increasingly, extreme popularity distributions across various media, including box office (Figure 23), demand for Netflix originals (Figure 24), streams on Spotify (Figure 25) and patrons on Patreon (Figure 26).

Figure 23. Distribution of Box Office Getting More Extreme

Source: Box Office Mojo, Author analysis.

Figure 24. Demand for Netflix Series Has Remained Skewed Despite Big International Expansion

Note: Parrot Analytics’ demand metric incorporates a variety of inputs to measure the popularity of series and movies. Source: Parrot Analytics, Author analysis.

Figure 25. The Head of the Spotify Curve Remains Extreme

Source: Spotify, Author analysis.

Figure 26. The Creator Economy Observes Power Laws Too

Source: Graphtreon, Author analysis.

These power law-like distributions are also evident when examining the payouts on self-distribution platforms. Here are just a few of many examples:

Linktree found that 46% of full-time creators make less than $1,000 per year.

Spotify has more than 11 million artists (as of 4Q21), but only 57,000 make more than $10,000 per year, or 0.5%.

Over 99% of Roblox developers make less than $1,000 per year.

Less than 0.25% of YouTube channels make money at all.

More Extreme Distributions Are Only Good for the Lucky Few

More extreme distributions have a lot of implications for the media business, which I also discussed in detail in Power Laws in Culture, but here are a few worth highlighting:

Bargaining power shifts to the head. The rare hit, and the talent behind it, has more bargaining power than ever.

Popularity is not necessarily a signal of quality, it’s a signal of what’s popular.

Luck matters. The idea behind these cascades is that people do what they see other people do. As a result, popularity is not always a signal of quality, it is a signal of what is popular. Popularity is unpredictable and “highly sensitive to initial conditions.” Luck plays a big role.

More variance means more risk. More skewed distributions mean more skewed financial outcomes. Just like in the financial markets, all things equal, higher variance means lower returns.

The lucrative middle is being hollowed out. If the head remains fat (or gets fatter) and the tail gets longer, it implies the middle of the curve has to get hollowed out. The middle is any media that was formerly successful because of scarce distribution that is no longer scarce. (Think middling TV shows on middling cable networks, indistinct local newspapers or radio shows, B-movies, etc.) Historically, this “middle” was lucrative for media companies. It is becoming less so.

A middle class may be elusive in the creator economy. In the last several years, numerous creator economy tools and platforms startups got funded in a bet that they could help foster a new creator middle class. The reality is that power laws are merciless and a creator middle class is more likely to result from better ways to monetize small audiences than less skewed distributions.

The last post explores the fourth trend, virtualization, and ties it all together.

This is a little redundant, since “information network” already implies “two way.”

The terms “positive” and “negative” feedback loops can be a little confusing. Feedback loops dictate how a system changes in response to a change in a parameter of the system. Positive feedback loops exacerbate the effect of the change in the parameter. Negative feedback loops dampen the effect of a change in the parameter. But positive feedback loops aren’t always positive and negative feedback loops are often not negative. In biology there are a lot of beneficial negative or homeostatic feedback loops - for instance, you sweat when you get hot to reduce your temperature. Similarly, a positive feedback loop could exacerbate an unfavorable trend, such as a social network losing users, which would trigger more users to leave. So, “reinforcing” and “balancing” feedback loops may be better terms, although they aren’t used as often.

OK, this is also confusing. Even though network effects manifest themselves as a supply-side dynamic (i.e., they concentrate power in few companies), they are referred to as demand-side economies of scale because the “demand side” (consumers) directly benefits from the scale.

Great insights, as usual.

As an entrepreneur in the "new media" (blast from the past word) space, I'm extremely curious in the creator middle class and monetization of small audiences.

I have convinced myself that niches and superfans is the way to go. So at Intercut, we are creating hyper-media (film, TV, and games, in parallell) franchises that we hope cater to niche audiences that has scale globally.

With tools that make our franchises fast to produce, we hope we get more swings at bat to test out new ideas, and see if those niches actually respond in a, potentially, scalable way.

The fun thing is you can go really deep. For instance, it's not just a genre like "Action Movies", but you can go down that rabbit hole and find audiences for niches/subgenres.

Globally there might be an engaged audience for "Hong Kong Action Movies" or "Assassins Action Movies".

Happy to get your thoughts, Doug.

/michael [at] intercut [dot] ai

one thing I wonder is the super sports app they have been talking about sense yesterday