The Year(s) Ahead in Media - Fragmentation

Falling Barriers, a Shifting Definition of Quality and the Splintering of Attention

Note: This is the first post of a four-part series.

Around this time of year, a lot of people publish their top predictions for the media industry for the coming year. As a bit of counter-programming, in this series I lay out a framework for value formation in the media industry over the next five-10 years.

The media business is noisy, but here I try to focus on what is enduring. I explore four trends: fragmentation (the splintering of attention); disintermediation (the declining bargaining power of traditional intermediaries); concentration (the role of networks in concentrating both power and attention); and virtualization (the blurring distinction between the physical and the virtual).

In 2024, the media industry will fixate on many topics: potential consolidation or change of ownership among Paramount, WarnerBros. Discovery and NBCU; the health of the overall ad market and continued divergence between traditional and digital; whether there’s another shoe to drop after the Microsoft-Activision deal; the resolution (or lack thereof) of succession planning and activist pressure at Disney; whether early buyers will still be using their Apple Vision Pros three months later; the rate of pay TV subscriber and linear ratings declines; the weakness of U.S. box office and whether it will ever show hope of reapproaching pre-pandemic levels; streaming video churn and profitability; whether growth will re-accelerate in the gaming market; regulatory and legal pressure on Alphabet, Apple and Meta; whatever Taylor does; Netflix’s continued forays into sports and gaming; the outcome of the NBA rights renewal and fate of local sports rights; the implications of Amazon entering the CTV ad market; the outcome of UMG/TikTok negotiations; what show/movie/album/game will be a surprise hit or flop; the fate of local news; industry-wide layoffs; and the blistering pace of advancements in GenAI, among many, many others.

All of these examples are manifestations of these four structural trends. They are tectonic in the most faithful sense of the metaphor—mostly unnoticeable day-to-day, but powerful, far reaching and (probably) unstoppable. Collectively, they make up the backdrop of operating in the media business today.

Tl:dr:

Media is mature because time spent with media is so high (in the U.S., more than half of non-sleeping time). Since time isn’t growing, overall value isn’t growing either. The key question is how it will be distributed.

The goal of this series is to establish a framework (ambitiously, a sort of “theory of everything”) for thinking about how value flows along the media industry value chain over time between creators, traditional intermediaries, new intermediaries and consumers. It comprises four tectonic trends: fragmentation, disintermediation, concentration and virtualization.

All these trends started with digitization. It was the Big Bang moment for modern media because it created a universal language for information goods and paved the way for universal innovations.

This post examines the first trend, fragmentation.

Fragmentation is occurring for two reasons: systematically declining barriers at each step of the content development process (production, marketing, distribution and monetization) have led to a near-infinite amount of content; and the very introduction of that content is changing consumers’ definition of quality.

An empirical look at fragmentation shows that while there is not much shift in time spent between media formats (video, audio, gaming, etc.), there is significant fragmentation happening within each format.

GenAI will accelerate this trend by making high production values more accessible even for the most demanding content formats, like premium video and AAA games.

Value flows to scarce resources. As content becomes infinite, a few things become relatively scarce: attention; hits; first-party data; curation; community and fandom; IP and brands; marketing prowess; and IRL experiences.

In the next post, we’ll examine the second trend, disintermediation.

The Most Important Questions in Media Pertain to Shifts in Economic Value

The main question I’m trying to answer is how economic value will shift along the media value chain long term.

Why Economic Value?

Every constituency of a business (investors, employees, suppliers, customers, regulators) may have a different definition of value because they value different things. By “value creation,” I mean the economic value a company generates, the difference between the money it brings in and the money that goes out.

Regardless of one’s definition, everyone with even a passing interest in a business, industry or value chain should pay attention to changes in economic value creation. Those changes have real world consequences, they are self-perpetuating and economic value is the primary motivation for management actions.

Changes in economic value have real world consequences, they are self-perpetuating and preserving or growing economic value is the primary motivation for management actions.

Changes in expectations for economic value have real-world consequences. In the court of public opinion, the most commonly agreed-upon barometer of whether a company is winning or losing is its stock price performance or, if private, the progression of its private market valuations. Both are based on perceptions about changes in economic value creation. For a company, when expectations for economic value growth increase, good things happen: shareholders are thrilled; salaries and stock-based compensation go up; employee morale is great and it’s easy to attract talent; funding is plentiful; customers, suppliers and partners are more willing to risk their time, money, attention or reputation; management whole-heartedly invests in the future, both internally and externally (through M&A); companies are more likely to engage in prosocial behavior (acting ethically, adhering to regulations, funding socially beneficial projects); and CEOs are lionized or deified in the press.

When economic value consistently falls short of expectations or, worse, starts to shrink, it can get bad. Companies often take draconian measures to reduce costs, including cutting perks and salaries and conducting layoffs; they are more likely to cut corners with regulatory compliance, quality control and ethics; board members, who probably joined when times were good and were happy to go along for the ride, realize the reputational risk of being aboard a sinking ship and become much more active overseeing (and second guessing) management; the company also becomes either risk averse, tamping down investment, or risk seeking by pursuing desperate acquisitions; morale is horrible and it becomes very difficult to attract and retain top talent; customers, suppliers and potential partners are more leery of committing resources or incurring reputational risk; funding dries up and/or becomes increasingly costly; shareholders are out for blood; heads may roll at the top; the company may fall prey to activist investors fomenting for change or hostile acquirers; it may sell off pieces or the whole company from a position of weakness; and CEOs are vilified in the press, sometimes in a very personal way. In the absolute worst cases, they make a limited series about you, starring Jared Leto.

These changes are self-perpetuating. As implied by the above, increases in economic value spark a virtuous circle and decreases devolve into a vicious one. The latter especially; it is very difficult to reverse course once things start spinning the wrong direction.

Management’s top priority is to grow or at least preserve value. It follows that CEOs’ and boards’ top priority is to increase or at least preserve the value of their companies, for both the benefits of the organization and their own personal gains (which don’t always align). Almost all significant management actions can be understood and predicted through this lens.

In Media, Shift Happens

Companies increase their economic value when the pie is growing or they take a bigger share of the pie (or both). For media overall, the pie is no longer growing.

As mentioned, the aggregate economic value of the media industry (like all industries) is the difference between the money that comes in (revenue) and the money that goes out (costs). Revenue is a function of two things: units (how much time people spend consuming media) and price (which is, in turn, a function of what they are willing to pay for those experiences and the competitive dynamic). The fundamental problem is time spent.

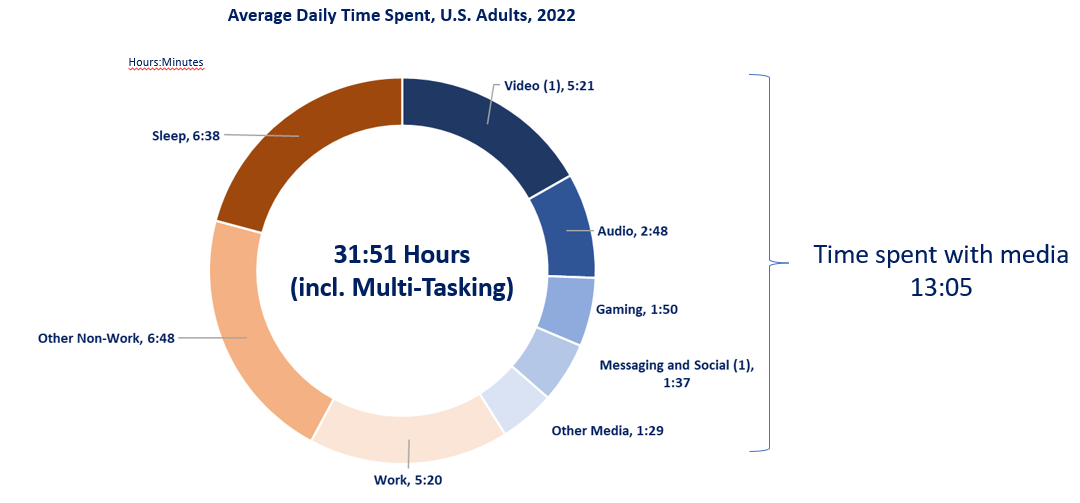

Everyone already consumes media, and a lot of it. As shown in Figure 1, according to consulting firm Activate, in the U.S., the average adult spends 13 hours per day with media, out of a 32 hour day (owing to multitasking). That’s 40% of total time and more than half of non-sleeping time. There is very little room for time spent with media to increase.

Figure 1. U.S. Adults Spend a Lot of Time with Media

Source: Activate analysis, Activate 2023 Consumer Technology & Media Research Study (n = 4,023), Company filings, Comscore, Conviva, data.ai, eMarketer, Gallup, GWI, Interactive Advertising Bureau, Music Biz, National Sleep Foundation, Newzoo, Nielsen, NPD Group, Omdia, Pew Research Center, PricewaterhouseCoopers, U.S. Bureau of Labor Statistics, YouGov.

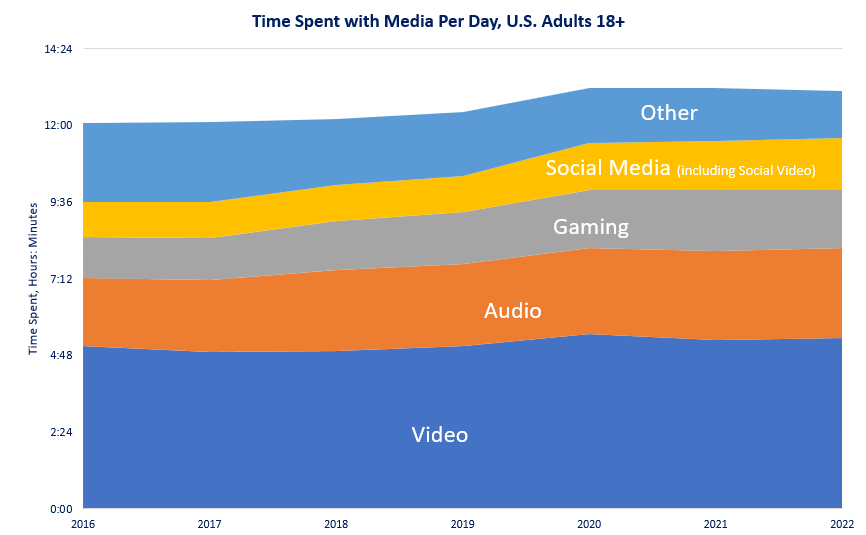

Another source for media time spent is eMarketer. It categorizes time spent differently, by device, not by activity, but it comes up with remarkably similar aggregate time spent, also a little more than 13 hours per day for U.S. adults (Figure 2). According to estimates from both Activate and eMarketer, time spent has sustained its pandemic-era bump, but is no longer really growing.

Figure 2. U.S. Adults Spend a Lot of Time with Media (Redux)

Source: eMarketer, April 2022.

The consequence is that globally, media and entertainment revenue is not growing on a real (inflation-adjusted) basis either. You can see this in Figure 3, which uses estimates from PwC and Omdia, both nominal and adjusted for inflation.

Figure 3. Globally, Media Isn’t Growing on a Real Basis

Source: PwC and Omdia, via Statista, IMF, Author analysis.

The only way for the aggregate revenue of the media industry to increase on an inflation-adjusted basis is if there is some fundamental change in the way consumers use media that encourages them to spend more time with media or pay significantly more for those experiences.

As a mature industry, the most important questions about media concern how value shifts along the value chain.

There are some reasons to be hopeful about that, as I’ll discuss later (part 4). The reasonable baseline assumption, however, is that the aggregate real value of the media industry is no longer growing. The most important questions about the industry therefore concern how value is shifting along the industry value chain1 and, to a lesser extent,2 between media verticals.

A Media “Theory of Everything”

I recently made the mistake of reading The Fabric of Reality, by physicist David Deutsch. It wasn’t a mistake because it was a bad book (it is fascinating, if dense), but because it led to writing this series of posts.

In it, Deutsch aims to articulate a “theory of everything” for, as the title implies, reality. He argues that quantum theory, the theory of evolution, the theory of knowledge (epistemology) and the theory of computation “taken together form a coherent explanatory structure…[that] may already properly be called the first real Theory of Everything.” By theory of everything, he means that if you understood these four concepts, and how they interrelate, you could “understand everything that is understood.”

What are the big, enduring structural trends in media?

I think we all have a desire to make order of things, or at least I do. I also find that the media business is so noisy that I need a framework to try to make sense of it. For me, reading The Fabric of Reality raised the question: is there a “theory of everything” for media? A few fundamental concepts—together, a mental model—that have both explanatory and predictive power, so that if you understood them and how they interrelate, it would enable you to understand the most important changes occurring in the media industry, filter out signal from noise and predict with greater confidence what will happen?

Good models should change when they encounter relevant new information, but my best answer today is that there are (coincidentally also) four concepts that, taken together, help explain and predict the most important changes occurring and likely to occur in the media business over the coming years: fragmentation, disintermediation, concentration and virtualization.

Before getting to the trends, a few words about the enabler of all of them: digitization. At the risk of stretching the analogy between the universe and media past the breaking point, digitization was modern media’s Big Bang.

The Big Bang: Digitization

All media is a representation of sound, images and text. In nature, sound and images are analog, varying in intensity continuously. (Text is neither digital nor analog.) Prior to widespread adoption of personal computers, CDs and the JPEG format in the 1980s, media was also (mostly) analog. Sound was recorded by replicating an analog waveform on a physical medium, such as by etching the pattern on vinyl or magnetizing iron oxide particles. Images were recorded by exposing light-sensitive paper to light, capturing the full range of tone (and eventually) color of the original image. Text was printed on paper.

So, the atomic units of all media were different: for a song, it was the note or maybe a waveform; for a film it was a frame or perhaps the individual grains on the photographic paper; for text it was the letter. There was no common language between them.

Digitization involves sampling an analog sound wave or image, “quantizing” it and converting that quantity to binary code, comprising bits. For text, it involves converting letters to binary code, also comprising bits. Digitization made the atomic unit of all media the same: the bit.

Digitization made the atomic unit of all media the bit, paving the way for everything that has followed since.

Bits have universality, in the sense that they are the standard unit for representing, processing, storing and transporting all digital information, regardless of the source, application, device, medium or communications network. This standardization of all media paved the way for all innovation that has followed since.

1. Fragmentation: Falling Barriers and a Fluid Definition of Quality

Media fragmentation is taken as a given. It’s intuitively obvious in our daily lives that our attention is spread between more songs, shows, reels, shorts, posts, blogs, etc., than ever. But it is also intuitively obvious that our attention is not evenly spread among all that stuff. Culture still coalesces around hits, whether Beyonce, The Bear, Mr. Beast or Barbie (an apparent contradiction I’ll try to reconcile in part 3).

To form a view whether fragmentation will continue, at what pace and the implications, it’s worth understanding why fragmentation is happening and, to the extent possible, monitoring it.

Why is Fragmentation Happening?

Fragmentation is occurring for two reasons, one supply side (lower barriers) and one demand side (a changing consumer definition of quality):

Infinite Content

Consumers face practically infinite content choices because the barriers to making it have been falling for two decades. Let’s talk about those barriers.

The product development process for all media products is roughly the same, whether an article, song, TV show or game. It starts with an idea, it must be produced, then marketed, distributed and monetized. Then, it is consumed3 (Figure 4).

Twenty years ago, production, marketing, distribution and monetization of media goods were all difficult and expensive.

Production often required expensive professional recording equipment and dedicated studios, complex workflows or powerful workstations and physical production and packaging of each newspaper, magazine, CD, cassette, DVD, film reel or game disk.

Marketing usually meant spending heavily on paid media, namely print, TV, radio and outdoor and sponsorships and earned media, which mostly meant public relations and publicity tours.

Distribution involved physical distribution to retailers, newsstands, movie theaters and radio stations or electronic distribution (such as over a satellite) to cable headends or satellite uplink facilities.

Monetization meant selling goods or subscriptions through an expensive (and often capital intensive) distribution network, billing and customer support and, for ad-supported media, selling advertising required a dedicated salesforce.

Figure 4. The Universal Media Product Development Process

Source: Author.

Over the last two decades, technology has reduced the cost of all of these steps, to varying degrees, in the following order.

As described, digitization created a standard atomic unit for all media products (and, for that matter, all information goods): the bit. The universality of bits means that innovations in the storage or transport of bits benefited all media. By creating one global, open network, the Internet unbundled information from costly infrastructure. Coupled with subsequent advancements in networking technology (broadband infrastructure deployment, compression algorithms, more efficient network topologies, etc.), the costs to distribute those bits plummeted to something close to zero.

Then, the lower barriers to develop owned marketing channels (such as websites, social followings and email distribution lists) lowered marketing costs.

The rise of self-distribution platforms like app stores, YouTube, Spotify, Steam and Substack democratized and simplified monetization.

Barriers to production have not fallen uniformly across all media, because some are much more complicated and expensive than others. One person can write a book or article or produce a song, while it takes hundreds or thousands of people to produce a premium TV series, film or AAA game. Nevertheless, innovations in content creation hardware (like embedding high quality cameras in phones), editing software (CapCut, Logic Pro, Adobe Premier Rush, etc.) and creation tools (like native tools in TikTok and YouTube, development platforms like Unreal and Unity) dramatically reduced production costs for independent creators and small teams.

Hence the explosion in content. To get a sense, check out the comparisons in Figure 5.

Figure 5. Falling Entry Barriers Have Resulted in a Content Explosion

Source: Author estimates, YouTube upfront May 2019, Tim Queen, Spotify 4Q21 earnings release, Spotify "Loud&Clear" Top Takeaways 2022, Wikipedia, Steam, Business of Apps.

A Changing Consumer Definition of Quality

Like the proverbial tree falling in the woods, this vast supply of content only causes fragmentation if people consume it. Under traditional standards of quality, a lot of the content enabled by these falling barriers doesn’t measure up. But people are consuming it because many consumers’ definition of quality is changing, at least some of the time.

“Quality” is the weighted set of attributes that consumers consider when choosing between identically priced goods. And it is always changing.

I’ve written about this idea before, most recently in What is Scarce When Quality is Abundant. You can think of “quality” as a (somewhat mysterious) algorithm. It is the weighted set of attributes that consumers consider when choosing between identically priced goods. A convenient thing about this definition is that it is based on revealed preference, not stated preference. When consumers make different choices than they did in the past under similar circumstances, it reveals that their definition of quality has changed.

Media executives tend to have a relatively static definition of quality, but the consumer definition of quality is much more fluid, especially for younger consumers, who’s definitions are less ingrained. The attributes that define quality, and their respective weightings, change over time. If new entrants introduce new attributes that consumers value and internalize—even if only in some contexts, for some use cases—it changes the algorithm.

To make this more concrete, I often use hotels as an example. Prior to AirBNB, the traditional definition of quality might have included attributes like a central location, cleanliness, on site dining options, level of customer service, brand, generosity of loyalty programs, 24-hour room service and other amenities, like gym, pool or spa. AirBNB listings usually offer few of these, but they’ve introduced new attributes, like location in a residential neighborhood, privacy, a working kitchen, room to entertain, easy parking and more closet space. For some customers, these attributes are now important attributes of quality. That’s not to say that the previous attributes no longer matter at all, but the inclusion of new attributes definitionally reduces their importance.

To bring it back to media, it is self evident that this shift is underway. Younger consumers may collapse on the coach and scroll through TikTok or Instagram Reels for an hour without even thinking of turning on the TV. But it’s happening for older consumers too. Hardcore gamers who occasionally play casual games; TV watchers who sometimes opt for YouTube; newspaper readers who subscribe to a few Substacks; or radio listeners who also listen to underground artists on Soundcloud, are all exhibiting a changing definition of quality.

An Empirical Look at Fragmentation

It’s tough to quantify fragmentation. There is no single view of consumer time spent by activity across all media formats. Cobbling one together requires aggregating many disparate data sources that use different methodologies, including a mix of survey and observational data. So, the data aren’t internally consistent and self-reported data in particular are usually flawed.

As noted above, Activate publishes a comprehensive view of time spent with media each year, by media format. It has some limitations, because it is also an aggregation of different data sources, it only measures behavior in the U.S for adults over 18 (overlooking younger consumers, who use media very differently and are usually a leading indicator of the broader population) and it isn’t necessarily meant to be used longitudinally, because the methodology can change a little year-to-year. But it’s a start.

Figure 6. Time Spent Has Not Shifted Materially Among Media Verticals

Note: “Video” includes YouTube viewing on TVs, but excludes “social video.” “Social Video” includes YouTube mobile, TikTok, Facebook, Instagram, Twitter/X, etc. Source: Author analysis of Activate data.

Activate assigns media usage to five categories: video, audio, gaming, social media and other. A time series of this data shows relatively little change in time spent between these categories (Figure 6). As highlighted in Figure 7, from 2016 to 2022, video has maintained its share of usage and audio, gaming and social are all up a few points. The “other” category, which comprises reading, web browsing, going to the movies and live events, is the only clear loser.

Figure 7. Video Has Maintained Share and Audio, Gaming and Social Media (Including Social Video) Have All Gained Share

Source: Author analysis of Activate data.

These relatively modest shifts aren’t that surprising because each of these broad categories is a relatively distinct use case—even if there is clearly some bleeding happening between them. People watch long-form video when they can allocate a decent slug of time (at least 20 minutes); they often listen to music or podcasts when multitasking or commuting; they play PC or console games when they have even more time and want to deeply engage with something, etc. What this high-level view fails to capture is the significant fragmentation happening within these categories.

There aren’t dramatic shifts between media categories, but there is significant fragmentation occurring within them.

Video

Each month, Nielsen publishes The Gauge, which shows how viewership is shifting on TVs in the U.S. As shown in Figure 8, over the last four years, streaming’s share of viewing on TVs has almost doubled.

Figure 8. Within Video, Streaming Share Has Almost Doubled Over the Last Four Years

Source: Nielsen.

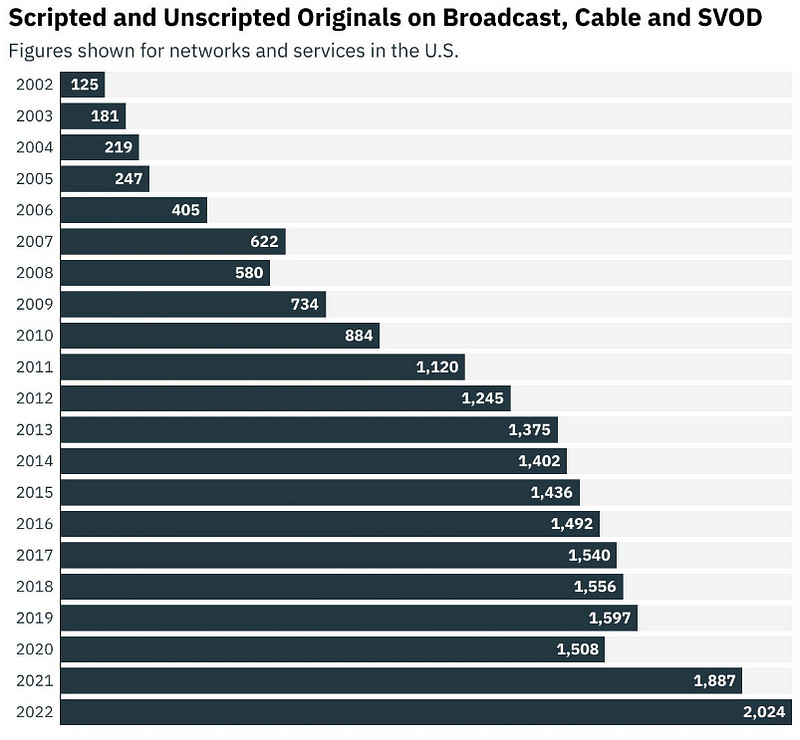

Some of this streaming viewing is just shows that are on linear networks consumed on a new medium, and therefore doesn’t qualify as fragmentation. But a lot of this content is new. All of the streaming services, including both non-traditional4 services (like Netflix, Amazon and Roku) and traditional streaming services (Hulu, Disney+, Max, Peacock and Paramount+) have invested heavily in exclusive original content. This can be seen in Figure 9. Over the last decade, the number of original series on broadcast, cable and SVOD has doubled.

Figure 9. Original Programming Has Almost Doubled in the Last Decade

Source: Variety Insight by Luminate, Variety Intelligent Platform analysis.

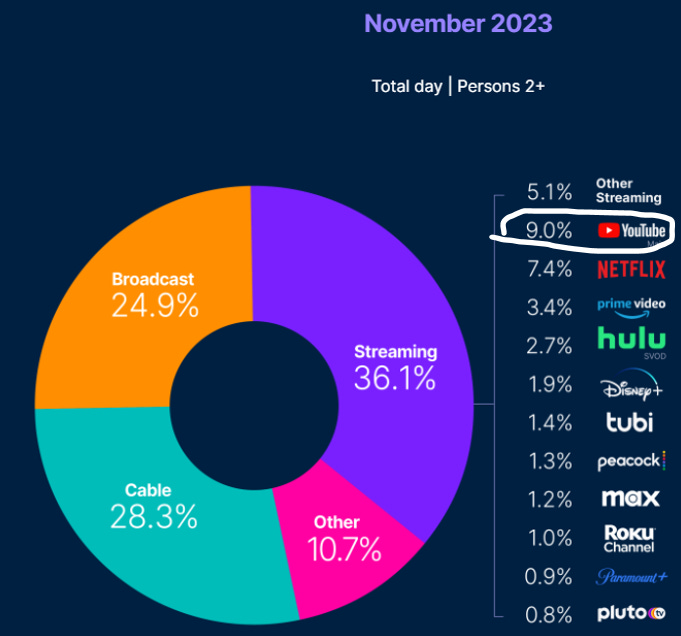

Also, keep in mind that the single largest streaming service on TV, as tracked by Nielsen, is YouTube (Figure 10). In November, for instance, nine percentage points of streaming’s 36% viewing share, or 1/4, was YouTube. All of that viewing represents fragmentation.

Figure 10. YouTube is the Biggest Streaming Service in the U.S. to TVs

Source: Nielsen

As mentioned, this Nielsen data only measures viewing on TVs and the only short-form5 video it captures is viewing of YouTube on TVs. It’s possible to get a fuller view of the impact of short form by combining this Nielsen data with Activate data. As noted above, Activate distinguishes between “Video” (which includes YouTube viewing on TVs) and “Social Video” (which includes YouTube viewing on mobile and video viewing on TikTok, Facebook, Instagram, etc.). Activate’s estimates for the usage of social video is shown in Figure 11. As also noted above and in the chart, this is only for adults 18+.

Figure 11. According to Activate, “Social Video” Has Been Growing Rapidly

Note: “Social Video” includes time spent on YouTube mobile, TikTok, Facebook, Instagram, Twitter/X and other social platforms. Source: Activate.

Using the Nielsen data in Figure 10 (and adjusting it to exclude kids 2-18 viewing), we can move the YouTube viewing on TVs from “Video” to “Social Video” to get a better (if still rough) picture of total time adults spend with short-form video (Figure 12). As shown, based on this analysis, short form now represents an estimated 1/4 of all video viewing for adults, up from <15% four years ago.

Figure 12. Short Form is Now ~25% of All Video Viewing for Adults

Note: “Long Form” could alternatively be called “professionally-produced” or “Hollywood” content; “Short Form” is sometimes called “user-generated” video or “social” video. Source: Author analysis of Nielsen and Activate data.

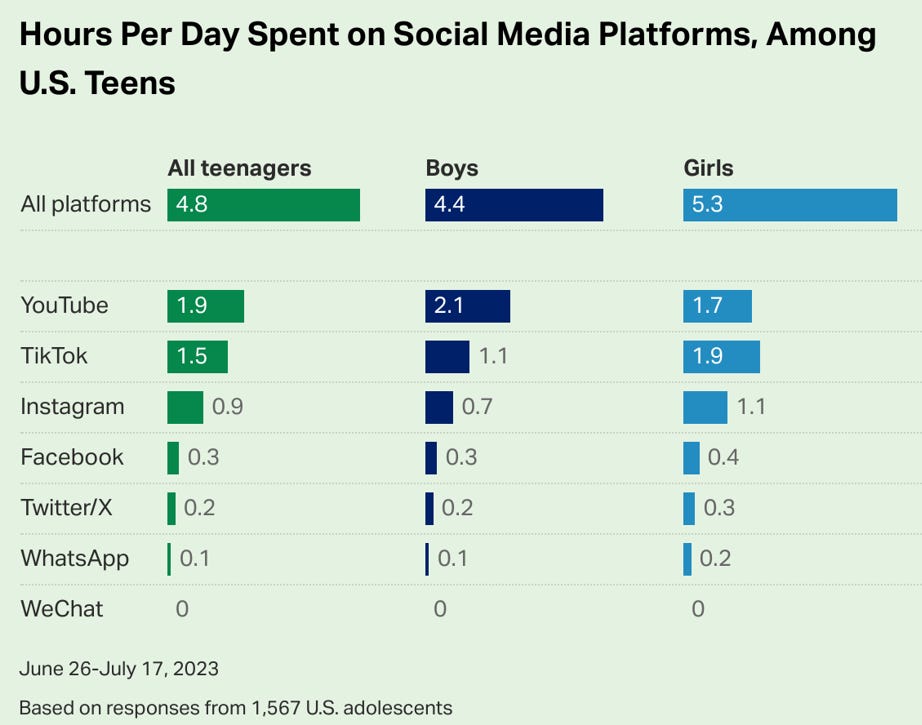

To state the obvious, kids’ engagement with short form video, which isn’t captured in Figure 12, is far higher. According to a recent Gallup poll, U.S. teens are consuming close to five hours of social media per day, almost all of which is video (Figure 13).

Figure 13. Short Form Viewing is Substantially Higher for Teens

Source: Gallup

Audio

According to the Activate data shown in Figure 6 above, time spent with audio has been growing over the last several years. But there is fragmentation within this category too.

Figure 14 shows Spotify data on the proportion of streams each year attributable to the major labels and Merlin (which manages rights for over 30,000 independent record labels). Considering that Spotify has over 11 million artists on the service, of which 98% aren’t represented by a label, the majors and Merlin have been pretty resilient. But their share of streams declines every year.

Figure 14. The Majors and Merlin Have Proved Resilient, but Lose Share Every Year

Source: Spotify Form 20-F.

Also, according to Edison Research, average daily podcast listening for in the U.S. (for everyone 13+) has grown by 20 minutes over the last decade, up five-fold (Figure 15). Activate data shows time spent with audio up about 40 minutes per day since 2016 — so, the implication is that roughly 1/2 of the increase in audio time spent over this period is due to growth in podcast listening. That is also fragmentation.

Figure 15. Daily Podcast Listening is Up About 20 Minutes Per Day

Source: Edison Research.

Gaming

It’s hard to find reliable information on time spent with different gaming categories, but revenue is a useful proxy. As shown in Figure 16, over the last decade, mobile has grown from a rounding error to almost half of all gaming revenue. Given the prevalence of free-to-play in mobile, it’s a reasonable assumption that mobile monetizes at a lower rate per hour of consumption than PC or console. If right, that would imply that mobile is now well more than half of all time spent with games.

Figure 16. Mobile is Half of All Gaming Revenue and Probably Even More of Time Spent

Source: Morgan Stanley.

And while supply doesn’t necessarily equate to fragmentation, supply of games is growing rapidly, especially independent games. Figure 17 shows annual game releases on Steam, which exceeded 14,000 last year.

Figure 17. There Were >14,000 New Games Released on Steam Last Year

Source: SteamDB

Will Fragmentation Continue and What’s Scarce Now?

This leaves us with two questions: will attention continue to fragment and who benefits?

GenAI could pull down the last barrier in the content product development process.

There is good reason to think that fragmentation will accelerate. As noted above, technology has been systematically reducing the barriers to distribute, market, monetize and produce content for years. Of these, production has been the toughest nut to crack, especially for the most expensive and complicated forms of media. The advent of GenAI could pull down this last barrier by democratizing high production value creation of video, music and games and blurring the quality distinction between professionally-produced and independent/creator content. (I’ve written a lot about that over the past year, including Forget Peak TV, Here Comes Infinite TV, How Will the “Disruption” of Hollywood Play Out?, AI Use Cases in Hollywood and Is GenAI a Sustaining or Disruptive Innovation in Hollywood?.)

One of the foundational assumptions of microeconomics is that value flows to scarce resources. And when one input becomes relatively more abundant, other inputs become relatively scarcer. A few months ago, I wrote a piece called What is Scarce When Quality is Abundant that, as the name implies, attempted to lay out what becomes scarcer as content approaches “infinite.” (Another way of thinking about this: what filters will consumers use when facing infinite choice?)

Consumer time and attention. As content supply continues to grow faster than time spent with media, consumer attention becomes scarcer.

First-party data. As fragmentation continues and the constraints on using third-party data increase (post-GDPR/App Tracking Transparency/Google cookie deprecation), having first party data, at scale, is arguably more valuable and scarcer than ever. Data will likely be a—if not the—key source of competitive advantage in curation and marketing (among other things), mentioned below.

Hits. Faced with infinite choice, consumers will increasingly use popularity as a signal of quality and social currency (as I discuss in part 3). These hits will be more valuable than ever, but they will be extraordinarily rare and, because they often emerge organically from the network, they are unpredictable and require a lot of luck.

Curation. Consumers will also sometimes use recommendation systems as filters, depending on the use case and opportunity cost of sampling recommended products.

Fandom and community. Some consumers will select content based on their desire to be part of a community.

Brands and premium IP. When confronted with infinite choice, consumers will sometimes gravitate to brands and IP they know or even just recognize. But this requires balance for rights holders, because it is easy to over-exploit IP and create “franchise fatigue.”

Marketing prowess. With so many other signals influencing consumer decisions, paid marketing has become less effective. But, for the same reason, marketing that can cut through the clutter—such as by germinating, amplifying or dampening the signals that organically emerge from the network, as appropriate—is more valuable than ever.

IRL experiences, including sports. Technology hasn’t replicated the thrill or commoditized the scarcity of a live event, at least not yet.

The next post turns to the second fundamental trend, the disintermediation of traditional intermediaries.

The term “value chain” originally referred to the activities within a company to take a product from inception to delivery, but in recent years has been expanded to include third parties involved in this process, sometimes referred to either as an “industry value chain” or “value system.” I sometimes use “value chain” as shorthand for “industry value chain.”

It is “to a lesser extent” because time and dollars are not shifting dramatically between verticals, as I’ll discuss later in this section.

The term “consumed” is a misnomer. Media products are considered “non-rivalrous.” Since one person using a digital media product doesn’t reduce the supply of that product, they are never actually consumed.

By “non-traditional,” I mean the newer entrants that aren’t affiliated with linear broadcast or cable networks.

“Short-form” refers to non-Hollywood produced video, which is consumed primarily on YouTube, TikTok, Instagram Reels and other social platforms. It is alternatively called “user generated content (UGC)” or “social video.”

Super interesting, can't wait for parts 3 and 4. Good context for anyone looking for a framework of how media works today.

"Fandom and community. Some consumers will select content based on their desire to be part of a community."

Building this for Roblox, would love to show you the mvp.