What Will Streaming Peace Look Like?

Exploring possible structural changes in TV

[Note that this essay was originally published on Medium]

The streaming wars have not gone as planned.

From the beginning, very few people thought that every streaming service would “win.” It was never realistic that most consumers would subscribe to seven or eight separate general entertainment services.

What is newly evident over the last year is how hard it is to make money sub-scale and that, as a result, most mass market streaming services will struggle to be profitable at all. At the same time, traditional pay TV sub losses are accelerating, with no stabilization in sight.

Wars usually end when the opposing sides develop a sufficiently similar view of the likely outcome. We have arguably reached that point. So, what might Streaming Peace look like?

In this essay, I explore scenarios for what happens in the TV business over the next few years.

(One note: Last month, I posted an essay called Forget Peak TV, Here Comes Infinite TV. It argued that over the next decade, the barriers to create high production value content will fall as user-generated content continues to change the consumer definition of quality; virtual production and AI democratize high production value tools; and web3 makes financing more accessible. This essay addresses the near-to-mid term and does not contemplate those kinds of changes, which could be so disruptive as to render the industry almost unrecognizable.)

Tl;dr:

In the face of clear evidence that the streaming business will be neither as large nor as profitable as hoped for most players, the industry has collectively shifted its focus from subscriber growth to “optimization:” price increases, introduction of ad-supported tiers, moderation in the pace of content spend growth and many other incremental steps that can help improve profitability.

But what if that isn’t enough and the industry structure needs to change?

If the market simply can’t support seven or eight mass market streaming services, one of two things needs to happen, or some combination of both: Several need to merge and/or some players need to pick a lane between content and distribution. The former is a constant topic of speculation. The latter is not.

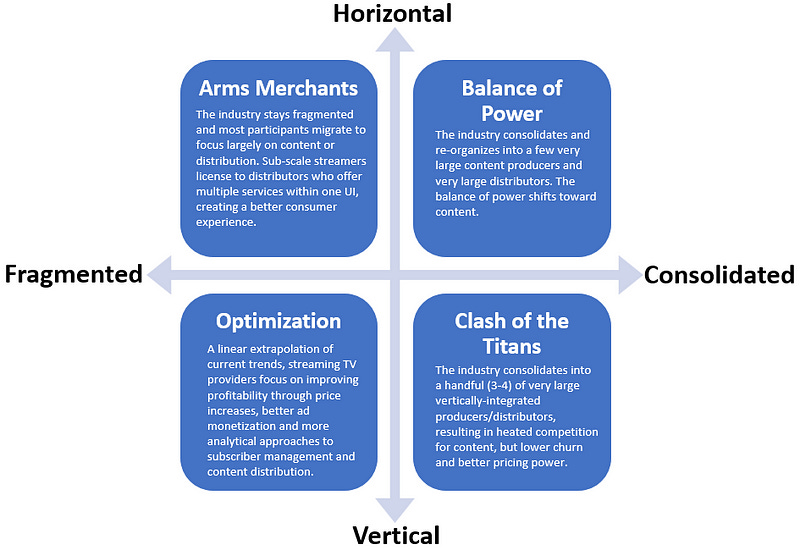

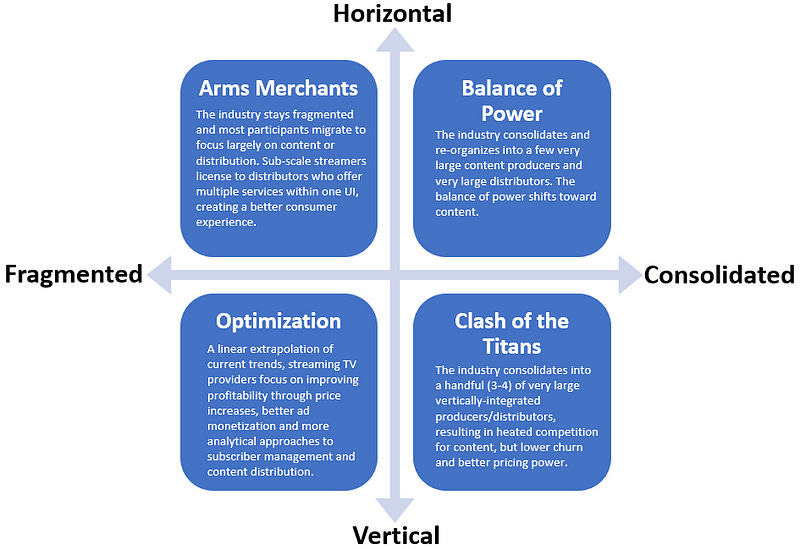

No one knows what will happen, but a useful tool for exploring the range of possible outcomes is a scenario planning matrix. Below, I present a 2 x 2 matrix which varies two variables between their logical extremes: industry concentration (fragmented vs. consolidated) and industry organization (vertical vs. horizontal).

I also provide a narrative for each of the four resulting scenarios: fragmented/vertical (“Optimization”), which is the status quo; consolidated/vertical (“Clash of the Titans”); fragmented/horizontal (“Arms Merchants”); and, representing the most extreme change, consolidated/horizontal (“Balance of Power”).

These are extreme by design. But the exercise helps define the bounds of possible outcomes; highlight the signposts that would indicate we are heading in one direction or another; and forces us to think through the implications of each possible future state.

The matrix is a little bit of a Rorschach blot, but I see three main takeaways: 1) the industry structure needs to change, optimization isn’t enough; 2) a gradual shift towards more horizontal organization is more likely than substantial consolidation; and 3) Netflix is in the catbird seat in any scenario.

Things are Not Good

If you follow the industry, you’re aware that the streaming business has proved a lot tougher than many expected, especially for the traditional media companies. Most telling is the scale of losses. As shown in Figure 1, last year the four largest traditional media companies, Disney, Comcast (NBCU), WarnerBros. Discovery (WBD) and Paramount, collectively lost more than $10 billion on their streaming efforts, with both Paramount and NBCU forecasting higher losses in 2023.

Figure 1. The Largest Entertainment Companies Likely Lost >$10 billion on Streaming Last Year

Notes: (1) Disney on Sept. fiscal year. (2) 2022 estimated based on YTD through 3Q22. Source: Company reports, Author estimates.

Contrary to perception, this is not just about content costs and it is not just a scale problem that you can “grow out of.” For some streamers, the unit economics don’t work. As I have written before (see Is Streaming a Good Business? and To Everything, Churn, Churn, Churn), examining Netflix’s unit economics show that, even at scale, the non-content costs of running a streaming service are very high.

Operating expenses include a lot of components that weren’t necessary to run wholesale linear channels, like content delivery (through a CDN), digital rights management, recommendation systems, subscriber management systems, customer service and support, session monitoring and management, account management, billing, payment systems, and, of course, the UI itself, which requires continuous refinement and A/B testing. Churn management is also very expensive. As shown in To Everything, Churn, Churn, Churn, based on current high churn levels, I calculate that maintenance marketing costs alone— or what you can think of as churn replacement cost — may chew up 1/3–1/2 of ARPU for some streamers.

At the same time, there are no signs that the traditional linear business is stabilizing. It is possible to show that in a lot of ways too, but rather than beat a dead horse, I will just show MoffettNathanson’s calculation of quarterly pay TV sub growth, which requires no comment (Figure 2).

Figure 2. There is No Sign of Stabilization in Pay TV Sub Declines

Source: MoffettNathanson.

Is Optimization the End Game or a Temporary Equilibrium?

In the light of this increasingly stark evidence, in recent months the industry has shifted its focus from streaming subscriber growth to profitability or “optimization” (see Media’s Shift from Growth to Optimization).

Many of the industry’s recent steps could be categorized as optimization: price increases by Netflix, Disney and HBO Max; Netflix’s efforts to curtail password sharing; Netflix’s decision to moderate the pace of content spend; the move to offer ad tiers by Disney and Netflix; WBD’s stated intention to embrace theatrical distribution; the repurposing of HBO originals on TNT and tbs; NBCU cost cutting in its linear networks; layoffs at AMC, etc.

In Media’s Shift, I laid out a bunch of potential additional optimization actions, which fall under the categories of monetization, acquisition/retention, cost (particularly content optimization) and portfolio (Figure 3). This is easier said than done. By definition, optimization means making different decisions for different content assets, customers and distribution channels, in different contexts. Today, most media companies aren’t equipped to make these decisions in a systematic way. I expect that over the next few years, the industry will invest in the necessary analytical tools and institute decision rules that make it possible to optimize at scale. That won’t grab a lot of headlines, but over time it should help improve profitability.

Figure 3. There are a Lot of Things to Optimize

Source: Author.

But this raises a question: “Is this enough?”

Or, to ask it differently, if the market simply cannot support seven or eight different streaming services, does the structure of the industry ultimately need to change? And if so, how?

Why Scenario Analysis?

No one knows whether the industry structure will change meaningfully. Even the people who are best positioned to shape that future — Bob Iger, Reed Hastings/Greg Peters/Ted Sarandos, Brian Roberts, David Zaslav, Shari Redstone and their bankers — don’t know, because they can’t predict or control for all kinds of unknowns, like potential competitive actions, capital market receptivity or the regulatory environment.

Even in an uncertain environment there are tools that can help us frame out the potential outcomes. One of these is a scenario planning matrix. This entails identifying the two critical variables of a question, varying these two drivers between their extremes and constructing a 2 x 2 matrix that produces four potential scenarios. The most instructive part is writing a narrative describing each of these scenarios.

The goal is not to find the “right” answer. The scenarios are extreme, by design, so reality will probably fall somewhere between them. But the exercise helps define the bounds of what will probably unfold; the markers that would indicate we are heading in one direction or another; and the potential implications of different outcomes (including the strategies that would be optimal in each case and the dominant strategies that would succeed across multiple scenarios).

Two Axes: Concentration and Organization

Today, the streaming TV business comprises seven or eight vertically-integrated producer/distributors selling (essentially) exclusive general entertainment services direct-to-consumer: Apple (Apple TV+), Amazon (Prime Video), Comcast (Peacock), Netflix, Paramount (Paramount+ and Showtime) and WBD (HBO Max and discovery+, which they will reportedly combine soon). And with YouTube’s recent investment in the NFL Sunday Ticket rights, maybe eventually we’ll be able to throw YouTube in there too. (On top of that are dozens of niche streamers, like AMC+, BET+, BritBox, Curiosity Stream, Fox Nation, etc.)

It was never plausible that the average household would buy seven or eight different general entertainment streaming services; what is becoming clear is that the disaggregation of the TV business is the industry’s central problem.

As mentioned above, no one thought that the average consumer would subscribe to seven or eight different services. Recently it has become clearer that this is not just an inconvenient truth, it is the industry’s central problem — it is highly inefficient for both suppliers and consumers.

A big part of the reason why streaming is unprofitable for all of the traditional media companies is the need to replicate the distribution infrastructure and subscriber management that used to be funded by pay TV distributors, as I described before. Having so many services is also a horrible consumer experience. Despite efforts to enable search across apps by CTV providers like Apple and Roku, deep linking into multiple apps is still klugey. Consumers also report growing “streaming fatigue” — confusion and frustration about the sheer number of choices.

The logical outcome is that there are fewer distinct services over time. To get there, one of two things needs to happen, or a combination of both: either the industry needs to consolidate or most players have to pick a lane and focus largely on either content production or distribution.

So, to explore how industry structure might evolve, the two variables I chose for the matrix are: 1) degree of industry concentration and 2) nature of industry organization (i.e., whether it is predominantly organized vertically or horizontally).

The former is a constant topic of speculation and for good reason. The media industry (like most industries) has a long history of consolidating. The latter is not, so let’s spend a minute here. Over the last few years, the entertainment companies have made massive investments in distribution infrastructure and digital distributors have made massive (albeit, relative to their scale, less massive) investments in content. On the face of it, the idea that most will reverse course may seem unlikely, but I think it’s a valid question for a few reasons:

Whether entertainment companies back away from distribution and distributors back away from content is a valid question.

The scenarios are extreme, but the transition could be happen in a gradual way through the reallocation of resources and possibly subtle strategic shifts. For instance, one option for some streaming providers would be to continue supporting their owned and operated (O&O) streaming services but also license them to other distributors, similar to what Paramount, Lionsgate (Starz!) and WBD do with Amazon Prime Video Channels. Over time, those third party distributors could represent more subs than their O&O services, effectively shifting these entertainment companies back to content producers/packagers and away from distribution.

Efforts to vertically integrate probably haven’t paid off as hoped. That’s obvious for most of the traditional media companies. It is also an open question whether Apple or Amazon have realized their goals with their content investments.

Most are sub-scale in one or the other. Perhaps other than Disney, all of the traditional entertainment companies are sub-scale in distribution. Among the new entrants, Apple and YouTube are sub-scale in content (especially YouTube). Amazon’s domestic spending is probably close to Netflix’s (it spent $7 billion globally last year, most of which is domestic, compared to an estimated $6 billion for Netflix domestically), but doesn’t have the viewership to show for it. The only company that has unequivocally achieved scale in both is Netflix.

The entertainment companies never wanted to be vertically integrated to begin with. For decades, arguably since the 1948 Supreme Court ruling that prohibited studios from owning theaters, the media conglomerates have primarily produced, acquired and packaged content. They didn’t distribute it. That only changed over the last few years with the launch of their streaming services. They reluctantly moved into distribution — over a decade after Netflix launched its streaming service — because they were scared of Netflix’s growing strength, the entrance of massive platforms and the increasing pressure on the traditional pay TV business. Regardless of how they might spin it now, none of them enlisted; they were drafted into the streaming wars by competitive forces.

None of the entertainment companies enlisted in the streaming wars, they were all drafted.

It’s happened before: see Music. Most people don’t remember that the music labels also attempted to launch their own streaming services. In 2001, Universal and Sony launched PressPlay and Real Networks, BMG, EMI and Warner Music (then part of AOL Time Warner) launched MusicNet. Sony tried again with Sony Music Unlimited in 2011. Ultimately, the labels realized that focusing on developing artists, owning IP and pitting Spotify against Apple and YouTube was a far more advantageous model. As another example of how the relationship between producers and distributors can shift, consider that all the major gaming publishers (EA, Activision, Ubisoft) distribute on Steam, something that would’ve been considered a crazy idea a decade ago.

Figure 4. Scenario Matrix for TV Industry Structure

Source: Author.

The Scenarios

With these two variables and their two extremes defined, we have a matrix with four scenarios (Figure 4). I named them “Optimization,” “Battle of the Titans,” “Arms Merchants” and “Balance of Power.”

Let’s stop here for a moment. The narratives describing each scenario are just sketches, of course. It’s impossible to think through all the second- and third-order effects. But the benefit of writing them is that it forces one to think through what would have to occur for each to emerge — which leads to conclusions about how likely each one is — and surfaces some of the implications of each. Maybe give it a try before reading on? I’ll wait.

OK, let’s keep going.

Here’s my version of the narrative for each.

Optimization — Low Concentration, Vertical Organization

Optimization describes the status quo, in which the industry stays relatively fragmented and organized vertically. In this scenario, there is no major additional consolidation and there remain seven or eight general entertainment streaming services. Why isn’t there any consolidation? Let’s say there is another Democratic administration in 2024, so the regulatory environment stays unfavorable. Besides that, the largest potential buyers decide that the upside of acquiring additional content production capabilities, library and rights is more than offset by the downside of increasing their exposure to declining linear networks. Consider one of the most-speculated combinations: NBCU/Sky and WBD. This probably isn’t possible until the two-year anniversary of the Discovery-WarnerMedia deal in April ‘24. A protracted regulatory review would probably delay close until spring ‘25. Then, another wrenching merger integration process probably puts us somewhere in ‘26 before the combined company is operating smoothly. What does the linear business look like by then?

Instead, the major players all pursue optimization, as described above. The media companies focus on improving the profitability of their own streaming services, selectively license content to third parties and rapidly reduce the cost structures of their declining linear networks. Streaming advertising proves a bright spot, as the combination of reach, brand safety and first party data enables streamers to offer the best of traditional TV and digital.

Nevertheless, with no alleviation of “streaming fatigue,” consumers remain price sensitive, churn stays high and streaming services-per-household stagnates at around the current level. With most of the entertainment companies’ streaming services only able to claw back their way to achieve marginal profitability and continued pressure on their linear businesses, most report stagnant or declining profits.

Battle of the Titans — High Concentration, Vertical Organization

In Battle of the Titans, the industry remains organized vertically, but becomes even more concentrated through a series of large mergers. This is arguably the consensus expectation of what occurs long term.

It’s a pick’em. Throw a bunch of entertainment industry trade articles and conspiracy-minded Wall Street reports into a LLM and see what IdleSpeculationGPT spits out: Comcast spins out NBCU and Sky into a separate entity and merges it into either WBD or Paramount; Amazon acquires whomever is left stranded; Netflix acquires Paramount for the studio, library and sports rights and converts CBS into a Netflix barker channel, etc. Or make up whatever you like, in whatever order you like. It is a little hard to see how all this could transpire from a regulatory perspective, but let’s play out the scenario.

Whatever the permutations, it results in a handful (let’s say four) very large, vertically integrated, global producers/distributors, each with their own D2C service. Each has sufficient scale that there is heated bidding for the most sought-after projects and rights on a global basis and content spend remains high. However, each also has sufficient scale to produce a steady stream of “must-have” content throughout the year and most streaming consumers (who are already taking ~4 streaming services today, on average) subscribe to all of them, causing churn to decline industry wide. With all services at relatively high penetration of streaming households, there is little incentive to compete on price, resulting in tacit collusion and attractive pricing power across the industry. The cable bundle is largely reconstituted, albeit disaggregated into a few different apps. The consumer experience doesn’t improve that much. Streaming operating margins never re-approach the halcyon days of the cable bundle, but they settle out in the low 20s.

Arms Merchants — Low Concentration, Horizontal Organization

Arms Merchants is the scenario in which the industry remains relatively fragmented, but most of the participants gradually transition to focus on either content or distribution. NBCU, Paramount and WBD not only license some content to other streamers, they also license their entire streaming services on a non-exclusive basis to third party distributors, including Apple, YouTube and Roku. They continue to sell Peacock, Paramount+ and HBO Max/discovery+ (respectively) on a standalone basis as a way of establishing a retail value, but over time a majority of their subscribers are sold on a bundled basis by third-party distributors. Although they must license their services to other distributors at a discount to provide a small margin and a bundled discount to customers, CAC/LTV is equivalent or even higher due to limited SAC and lower churn. Ultimately, they decide that the benefits of controlling every aspect of the customer relationship and retaining all first-party data are outweighed by the challenges of running these businesses sub-scale and benefits of wider distribution. (Plus, the first party data they retain through their O&O subscribers is sufficient to power their analytical models.) Streamers who were at risk of being rendered permanently sub-scale increase their distribution and are therefore able to continue to attract talent and projects.

These distributors join Amazon Prime Video Channels in aggregating multiple streaming services (which they may sell a la carte or bundled) within one UI, offering consumers universal search and recommendation and the ability to navigate to any content within one app. Disney must decide whether to stay exclusive, also license its services or seek to become an aggregator itself.

The elephant in the room here is Netflix. Again, these scenarios are meant to be illustrative. It is almost inconceivable that Netflix would revert to its historical role as distributor and abandon original programming. Instead, in this scenario Netflix would have to decide whether to act as aggregator in an effort to be “home to all television” or not risk diluting its current offering by adding other brands. Likewise, the big media companies would have to decide whether it is strategically foolish to license their services to Netflix.

In this scenario, the scales of bargaining power between content and distribution settle out somewhere in balance. Content providers are dependent on distributors to market their services, but the distributors also need a wide array of third-party content to attract subscribers. The distributors agree to more liberal data-sharing policies than has been the norm for large aggregators. The distributors rep all ad inventory on a programmatic basis, with advanced targeting, attribution and measurement, but the media companies retain the right to sell their own inventory (which they do when they can clear the programmatic price). With relatively similar offerings, distributors like Apple, Amazon and YouTube compete for customers through targeted investments in exclusive content, product quality and features and by bundling in other products and services.

The aggregation of most content in one app — the re-bundling of cable, albeit with more consumer choice — provides a better consumer experience and churn moderates industrywide.

Balance of Power — High Concentration, Horizontal Organization

Lastly, Balance of Power is the most extreme scenario, representing the most change. In this case, the industry both consolidates and re-organizes horizontally. You could call this the music scenario.

In this case, through a series of mergers and divestitures, there are only a few massive content providers (e.g., Disney, NBCU/WBD/Paramount) and distributors (e.g., Amazon, Apple and YouTube). Again, it is tough to see how regulators allow this to happen.

Overall, this scenario looks a lot like Arms Merchants, with the exception that bargaining power shifts somewhat to the content providers, who offer a more differentiated product and are able to extract greater economics (and data) from the distributors. Once again, Netflix has to decide whether to act as aggregator, in which it would probably have a big advantage over other distributors, or not.

Also similar to the Arms Merchants scenario, this results in a better consumer experience and lower churn.

What’s In that Rorschach Blot?

The matrix is a little bit of a Rorschach blot; you probably see in it what you are predisposed to see. For me, the primary takeaways are:

Something’s gotta give. Above, I posed the question: Is optimization enough? My answer is no, it is not. Relative to the status quo, every other scenario results in more efficient resource allocation on the supply side and a better consumer experience. Optimization may improve profitability, but it won’t resolve the underlying problem: there are too many separate services today.

A shift toward horizontal organization seems more likely than mass consolidation. If something has to give, especially for the sub-scale streamers, the question is what? They can certainly wait around in hopes of a merger or acquisition that would help resolve their scale problem, but the wait could be futile. The regulatory environment may not be accommodative. Even worse, over time potential acquirers may become increasingly gun shy about increasing their exposure to declining linear networks. Expanding distribution by licensing their services broadly may be the only way out. Whether Apple and even Amazon are committed to their current level of content spend long term is also an open question.

Netflix is best positioned in any scenario. As the only company with scale in both content and distribution, Netflix is in the catbird seat. Sure, its competitive position could weaken. Competitors could merge (either vertically or horizontally), putting it at a scale disadvantage. Similarly, other distributors could move to offer a wider array of third-party services, which might also give them a shot at becoming “the home for all TV” and displacing Netflix. But it has the most control over its own destiny, best positioning it to succeed in any scenario.