The Relentless, Inevitable March of the Creator Economy

How Big it Is and Why it Will Keep Growing at the Expense of Corporate Media

Imagine that from the time you were young, you worked hard to join a very exclusive, powerful club. Eventually, you made it, cementing your steadfast, lifelong belief that you, among very few, belonged there.

Then, another club opened next door. It let everyone in. It felt like a mockery of what you had achieved. But it kept growing, attracting more members, siphoning off more attention. Young people fantasized about joining that club, not yours. Your club now seemed stodgy and out of step. It would challenge some of your fundamental beliefs about yourself.

This describes how many in traditional media feel about so-called “creators.” They regard them as “less than,” crassly commercial, and certainly not artists. A recent dust up about The Hollywood Reporter christening a new Creator A-List is illustrative. As Justine Bateman tweeted at the time, this is a list “…of infomercial salespeople. It’s not Hollywood.”

Whatever one’s value judgments—whether the creator economy is a positive, democratizing force, or a bastardization of art and full of self-promotional hucksters, or something in between—numbers don’t lie. It is growing rapidly at the expense of traditional media and, as I explain below, will inevitably continue to do so.

Tl;dr:

Let’s subdivide the media and entertainment (M&E) market into the corporate media economy and the creator media economy. Since M&E overall isn’t growing much, the relationship between the two is mostly zero-sum.

Based on a bottoms-up analysis of the largest creator media outlets, I estimate that the creator media economy generated close to $250 billion in revenue last year, roughly 15% of the global M&E market. It is growing far faster and over the last four years accounted for almost half of global M&E growth. Conservatively, I estimate it will exceed $600 billion and 25% of global M&E revenue by 2030.

There are very powerful technological, cultural, demographic and economic reasons it could grow even faster than this:

1) Even absent GenAI, the volume of creator content should grow much faster than corporate media as creation gets ever more accessible;

2) GenAI will trigger a tsunami of creator content across media. Just as bits became the atomic unit to distribute information goods, tokens are becoming an atomic unit for the creation of information goods;

3) The quality distinction between corporate media content and the best creator content will continue to narrow;

4) Falling trust in institutions and rising demand for authenticity structurally favor creators;

5) Monoculture is in decline as consumers atomize into microcultures, disadvantaging the traditional media business model;

6) Demographics are destiny, and younger demos spend much more time with creator content; and

7) The current monetization gap for the creator media economy (the delta between time share and dollar share) should narrow over time.

All this is mixed news for creators and creatives. For traditional media, there are only two choices: figure out how to participate in the creator economy or accept a perpetually diminishing business.

This post is sponsored by WSC Sports.

The NBA, Top Rank, Euroleague and more are already working with the WSC Sports’ Creators Program to expand reach to fans and monetize archival and near live sports content.

Fans are following influencers, so give influencers official tools to provide new perspectives and storylines to their audiences. The Creators Program exposes your content to new potential fans and generates additional revenues.

WSC Sports’ Creators Program provides a turnkey solution for rights holders by offering:

Full rights holder control over content

Options for creator access and types of accessible content

Performance metrics and valuable data

Reach out to WSC Sports to learn more.

To contact me about sponsorship opportunities for The Mediator, reach me here.

Defining the Creator (Media) Economy

Let’s establish some definitions.

There isn’t a consensus definition of “creator.” Sometimes creators are considered synonymous with influencers. That’s relatively narrow, because it confines the creator economy mostly to Instagram, TikTok and YouTube. Sometimes creators are considered those who distribute content online strictly to commercialize it. On a recent episode of The Colin and Samir Show, Samir drew the distinction between a creator and a creative:

…a creator is someone with a distribution mind. They're thinking about what do I make that's going to reach the most amount of people? They're an independent media company….And they're trying to solve how they can get their content seen at a large scale on platforms…A creative is working on the craft, right? They're working on the skill set and they typically get hired to direct stuff or support other people in making their thing.

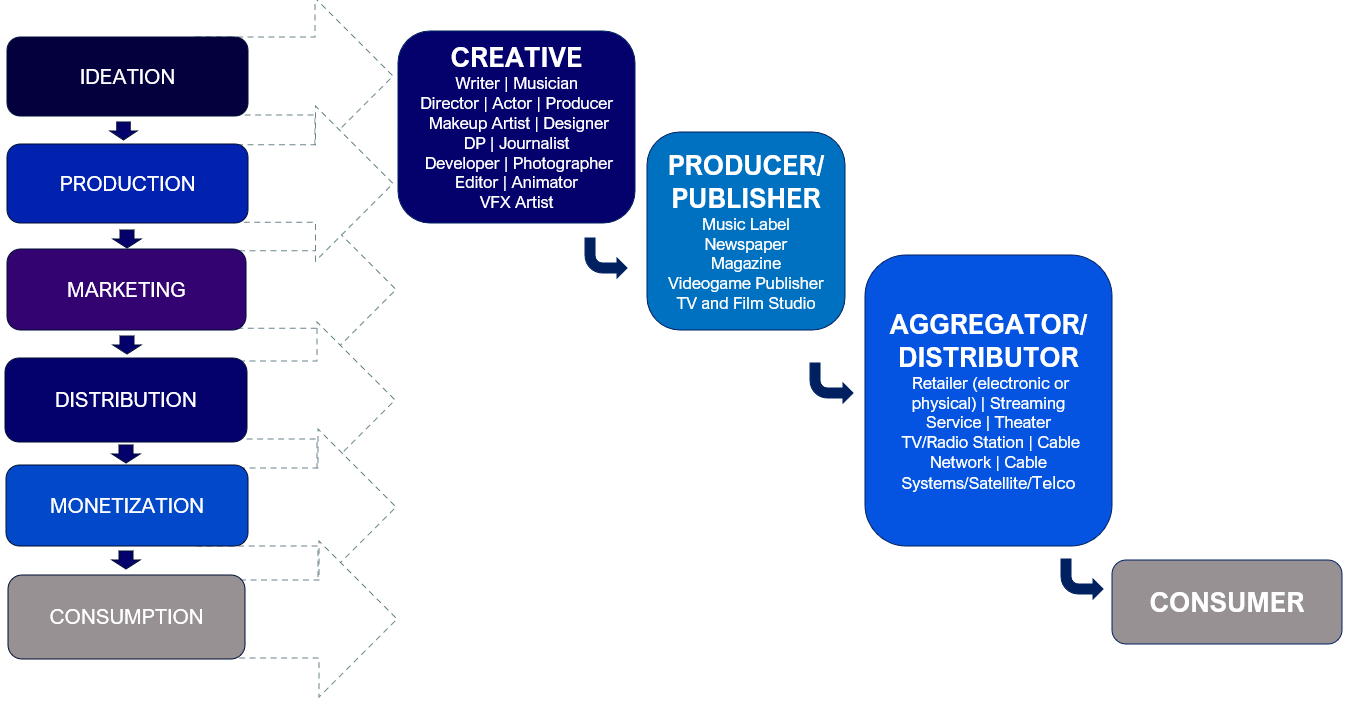

Figure 1. The Corporate Media Economy

Source: Author.

Figure 2. The Corporate Media Economy (Redux)

Source: Author.

Since I focus on the business of media, to me the most interesting distinction is between traditional media, or what we could call corporate media, and creator media. Let’s define two, mutually-exclusive, economies:

The corporate media economy is the ecosystem of traditional content creation, distribution and monetization, which usually entails institutional ownership, centralized decision making, portfolio-level risk management and several intermediaries between creative1 and consumer who provide financing, marketing and distribution (Figure 1). As shown in Figure 2, most of the household names in the media and entertainment business are intermediaries.

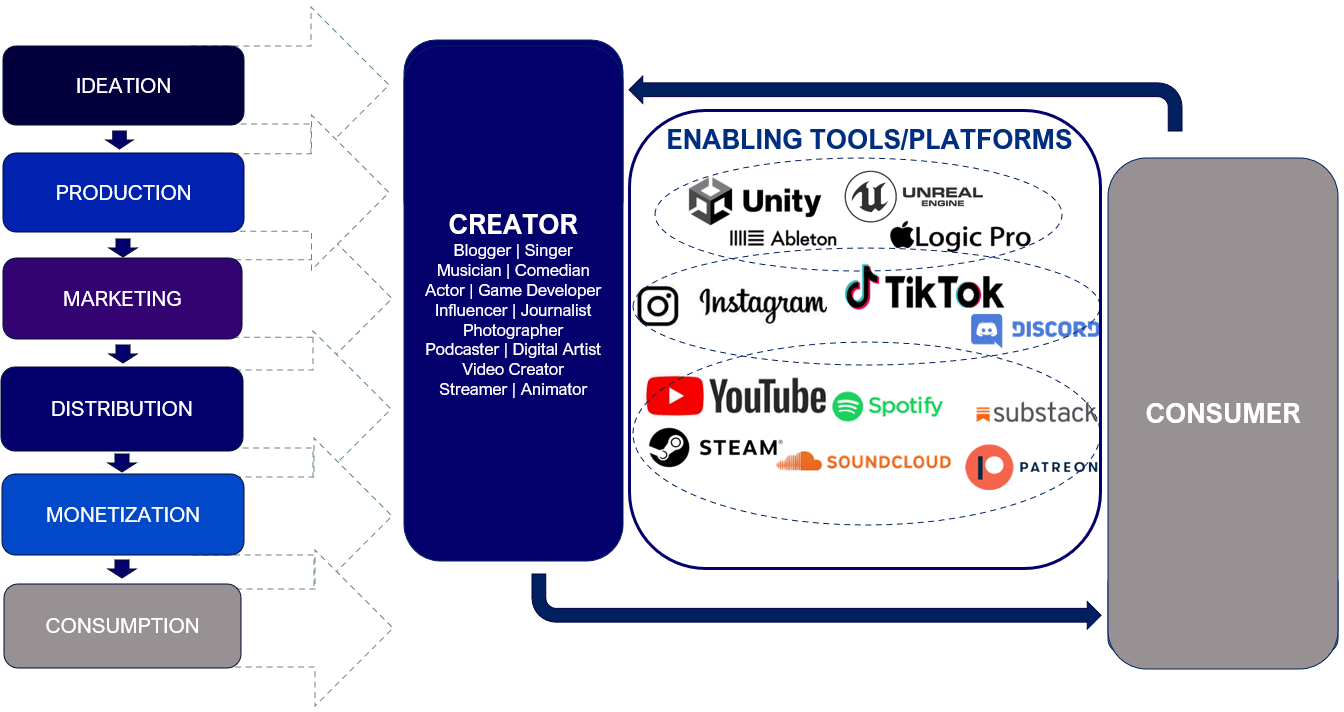

The creator media economy, as I’m defining it here, encompasses all other media monetization. It is the ecosystem of content creation activities in which independent creators create content on a self-directed basis, they have a direct relationship with consumers, and this content is monetized. The passive voice in the last clause signifies that the content is monetized by someone, even if not by the creators themselves. (So, under this definition, everyone who posts anything that generates revenue is a creator, even if it is Meta or X/Twitter who monetizes it, not them.) (Figure 3.) A gray area is small independent teams, of, say, 50 people or fewer. I put these in the creator category. Mr. Beast runs a full-fledged production company, with multi-million dollar budgets, but for these purposes he is a creator.2

Figure 3. The Creator Media Economy

Source: Author.

The Relationship Between Corporate Media and Creator Media is Zero Sum

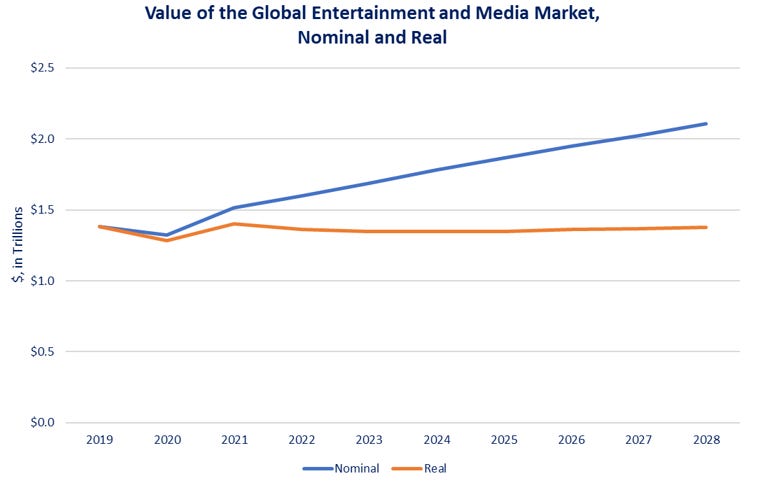

As I have written about before (like here and here), the overall media and entertainment (M&E) market is not growing much globally, slightly less than the rate of inflation (Figure 4).

Figure 4. Globally, Media Isn’t Growing on a Real Basis

Note: Includes PwC estimates for “Consumer” and “Advertising,” but not “Connectivity.” Sources: PwC and Omdia, IMF, Author analysis.

The reason is that time spent with media has stagnated in recent years. It grew with the advent of mobile starting in 2008 and then had a COVID bump in 2020, but has been flat or declined since (Figure 5). Since M&E revenue is derived by monetizing consumer time and engagement, it is tough for the overall market to grow faster than inflation if time spent is not growing.

Since M&E revenue is derived by monetizing consumer time and engagement, it is tough for the overall market to grow if time spent is not.

Figure 5. Time Spent is Not Growing Either

Source: eMarketer, April 2022.

As mentioned, my intention is that these two economies are mutually exclusive and cumulatively exhaustive (or MECE, as they say in consulting land). Every dollar of end-market M&E revenue is either one or the other. As there is only one pool of consumer time, the relationship between the corporate and creator media economies is largely zero sum. The growth in the latter mostly comes at the expense of the former.

Creators Generate Revenue on a Lot of Platforms

Under my definition above, creators’ work is monetized (there’s the passive voice again) on a wide variety of outlets and platforms. These include:

Social Networking (Meta, YouTube, Douyin, TikTok, Kuashiou, Snap, Pinterest, X, Bilibili, Weibo, VK, etc.)

Patronage/Community (OnlyFans, Patreon, Discord, etc.)

Gaming (Mobile Gaming, Steam, Epic, Roblox)

Livestreaming (Twitch, Bigo Live, Huya, DouYu)

Music (Spotify, Apple Music, Soundcloud, Bandcamp, etc.)

Podcasting

Influencer Marketing

Writing (Substack, Medium, Ghost, Beehiiv, etc.)

The proportion of total revenue on these outlets that is attributable to creators can range from very little to all of it.

For instance, in gaming, a relatively small proportion of mobile game (iOS and Google Play) revenue is attributable to independent developers (I estimate ~5-10%), slightly more for Epic, slightly more for Steam, and, for Roblox, almost all revenue is attributable to independent developers (other than the few games that Roblox creates itself). In music, Spotify reported that the major labels and Merlin accounted for 74% of streams last year, so we can attribute ~25% of revenue to independent and individual creators, but almost all of the revenue on Bandcamp likely comes from creators. On social networking and patronage platforms like Patreon, the majority or virtually all of the revenue is attributable to creators. Likewise, influencer marketing represents the sponsorship fees paid by brands directly to influencers and so is also 100% attributable to creators. This continuum of creator attribution can be seen in Figure 6.

Figure 6. The Proportion of Revenue Attributable to Creators Varies Widely

Source: Company reports, Author estimates.

How Big is It?

In Figure 7, I show my bottoms-up estimate of the aggregate end-market revenue of the creator media economy, i.e., all advertising, subscription and transactional revenue attributable to creator content, globally. I derived this by applying the proportions in Figure 6 to the reported or estimated revenue for each outlet. As shown, I calculate that total creator media economy revenue was a little shy of $250 billion last year.

Figure 7. The Creator Media Economy Approached $250 Billion Globally Last Year

Source: Company reports, eMarketer, Statista, Sacra, Wall Street Zen, Fast Company, Video Game Insights, MoffettNathanson, The Information, Influencer Marketing Hub, CB Insights, Music Business Worldwide, Author estimates.

Figure 8 compares creator media economy revenue to the total global M&E market, the nominal estimates shown above in Figure 4 (as estimated by PwC and Omdia). Last year, the creator media economy was almost 15% of the total $1.7 trillion M&E market (note that this includes what PwC calls “Consumer” and “Advertising,” but not “Connectivity”). It has also, obviously, been growing much faster. While PwC estimates that the total M&E has grown at 5% annually over the past four years, I estimate that the creator media economy has grown ~25% per year and corporate media has grown at 3%. So, although creator media is a relatively small portion of the total M&E market, it has accounted for almost half the growth.

The creator media economy has accounted for about half of total M&E revenue growth over the last four years.

Figure 8. The Creator Media Economy is ~15% of Global M&E and Half its Growth

Note: Global M&E includes PwC estimates for “Consumer” and “Advertising,” but not “Connectivity.” Source: Company reports, PwC and Omdia, eMarketer, Statista, Sacra, Wall Street Zen, Fast Company, Video Game Insights, MoffettNathanson, Influencer Marketing Hub, CB Insights, Music Business Worldwide, Author estimates.

The Creator/Independent Media Economy Will Inevitably Keep Taking Share

A simple math exercise shows how much larger and relatively more important the creator media economy will be by the end of the decade, if it keeps growing anywhere close to its recent pace.3 Presuming that the total M&E market grows in line with the PwC and Omdia estimate of ~4% through the end of the decade, then:

If the creator media economy grows at 10% annually, by 2030 it will be $460 billion and 20% of the M&E market;

If it grows at 15% growth annually it would reach $630 billion and exceed 25% of the market;

And, at 20% annual growth it would approach $850 billion and exceed 35% of the market.

Figure 9 shows the mid case, 15% annual growth.

Figure 9. The Creator Media Economy Could Easily Reach ~25% of Global M&E by the End of the Decade

Note: Global M&E includes PwC estimates for “Consumer” and “Advertising,” but not “Connectivity.” Source: Company reports, PwC and Omdia, eMarketer, Statista, Sacra, Wall Street Zen, Fast Company, Video Game Insights, MoffettNathanson, Influencer Marketing Hub, CB Insights, Music Business Worldwide, Author estimates.

Since no one likes wishy washy, let’s go with a point estimate: I forecast that the creator media economy will more than double by the end of the decade, exceeding $600 billion and 25% of the entire M&E market.

Powerful technological, cultural and demographic trends are tailwinds for the creator economy.

But there are a whole host of reasons—powerful technological, cultural, demographic and economic trends—why it could grow even faster than that. Let’s walk through them.

1. The Volume of Creator Content Will Keep Growing Fast (Even Without GenAI)

There is already a vast amount of creator/independent content.

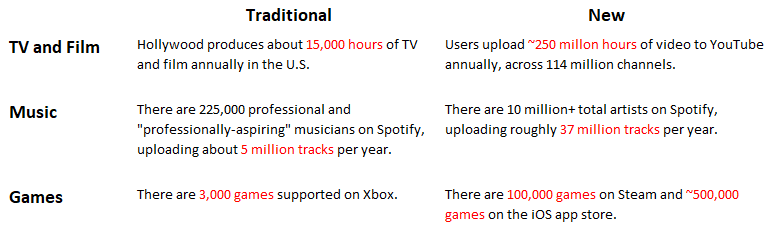

A few examples to make the point are shown in Figure 10. Consider: 20,000 times as much video is uploaded to YouTube each year as is produced by Hollywood (in other words, the equivalent of Hollywood’s annual output is uploaded every ~30 minutes, 24/7); 98% of artists on Spotify are hobbyists and they upload ~100,000 tracks per day; there are more than 30x as many games on Steam as are supported by Xbox (and it is set to add 17,000 new games this year).

Still, this gulf between the amount of creator content and “corporate” content will undoubtedly widen.

Figure 10. Some Examples of the Relative Scale of Creator Content

Source: YouTube upfront May 2019, Tim Queen, Spotify 4Q21 earnings release, Spotify "Loud&Clear" Top Takeaways 2023, Wikipedia, Steam, Business of Apps, Author estimates.

Part of the reason is that the more accessible it is to create, the more people create. Without probing the psychological or evolutionary roots of it, it is clear that humans have an innate desire to create. Closer to the bottom of Maslow’s hierarchy than the top, creativity emerges spontaneously in children (until it is wrung out of most of us by society, criticism or something else); throughout history, every known culture has produced art, music and stories; and people create art in the most extreme hardship, in prison, during war, and in dire poverty.

As evidence of this innate need, people create more when creation is more accessible.

The empirical evidence shows that people make more when creation is more accessible. Some examples:

While Kodak estimated that 80 billion photos were taken in 2000, current estimates are close to 2 trillion for this year, a more than 20-fold increase—obviously driven by the current constant availability of cameras.

YouTube has 2.7 billion MAUs and an estimated 114 million channels. Even if each of these channels is run by a discrete user and all of these channels are active (neither of which is true), that means about 4% of users also create. By contrast, TikTok makes creation much easier. It has a camera function in the app and offers in-app editing tools, filters, music libraries, text overlays, stitches, etc. According to a 2021 study by TikTok, 83% of users have posted a video.

In 2004, there were only a few thousand podcasts. Today, thanks to tools like Riverside FM, Zencastr, cheap webcams, high-quality mics and the like, there are currently over 4 million.

Through the natural progression of software development and the move toward no-code/low-code, creation tools will undoubtedly keep getting more user friendly: better and easier video editing tools; music sample and beat marketplaces and collaboration tools; no-code/low-code game development on UGC gaming platforms, etc. But the most significant innovation is likely to be generative AI (GenAI).

2. GenAI Will Trigger a Tsunami of Creator Content

If I were to distill the last couple of years of my writing into one sentence, it would be this: the last two decades in media were defined by the disruption of content distribution, facilitated by the internet, the next decade will be defined by the disruption of content creation, enabled by GenAI.

It not controversial to write that GenAI will result in a lot more content, but let’s tease apart the two key reasons.

Prior innovations in content creation technology have mostly reduced the cost for humans to execute creative decisions. GenAI reduces the number of creative decisions.

GenAI Automates Creative Decisions

Prior innovations in content creation technology have mostly made it easier and cheaper for humans to execute creative decisions. But they have not materially reduced the number of creative decisions. GenAI, in contrast, can automate creative decisions. Humans can decide what proportion of creative decisions they delegate to AI, anywhere from almost all of them to relatively few. (Whether the output in the former case will be any good is a different question.) But even when there is substantial human direction and oversight, it can automate a lot of creative decisions, dramatically speeding the creative process. (See GenAI is Foremost a Creative Tool for a more detailed discussion.)

As a General Purpose Technology, GenAI is Advancing Incredibly Fast

GenAI is clearly moving at a blistering pace. One of the key reasons this is happening is because it is a general purpose technology (GPT).

Most of the innovations in content creation over the last 5-10 years have been medium or domain-specific: ubiquitous cameras on mobile phones; cheaper in-home production equipment, like microphones; digital audio workstation (DAWS) software; free gaming engines for small developers from Epic and Unity; inexpensive and easy-to-use photo and video editing tools, etc. Advances in one domain didn’t necessarily benefit others. DAWs didn’t help anyone make videos faster.

Just as bits were a new atomic unit for the distribution of information goods, tokens are a new atomic unit for the creation of information goods—text, audio, images, video and more.

GenAI, like the internet, is a GPT. And just as bits were a new atomic unit for the distribution of information goods, tokens are a new atomic unit for the creation of information goods—text, audio, images, video and more.

It is hard to overstate the significance of the universality of tokens.

It is hard to overstate the significance of the universality of tokens. GPTs tend to advance much faster than narrow purpose technologies for many reasons: since they have such broad applicability, they attract orders of magnitude more resources (more capital, more labor, more brain power); breakthroughs in one domain (or modality) often benefit others; they tend to create new bottlenecks that lead to adjacent innovations (for instance, the compute and energy demands of GenAI will undoubtedly propel advancements in both); and wider adoption means a broader user base and a faster feedback loop. So, I don’t only mean advancements in the GenAI models themselves, but in tooling (like user-friendly interfaces and workflows) and integration with existing workflows and software. Like all technology, over time GenAI will get further abstracted away and will be seamlessly embedded in Adobe, YouTube Studio, TikTok, Soundcloud, Roblox, and probably ever other content creation tool and platform.

General purpose technologies tend to advance far more quickly because they attract a lot more resources; breakthroughs yield benefits across domains; they compel complementary innovations; and they benefit from a much faster feedback loop.

GenAI will greatly enhance current creators’ capacity to create and, probably, the number of creators too. It may feel like there are a lot of creators already, but 114 million channels on YouTube, 10 million artists on Spotify, 4 million podcasts or 80,000 developers on Steam are all miniscule relative to the potential global population of would-be creators.

3. The Quality Distinction Between Corporate and Creator Content Will Blur

The biggest knock against creator content is that it’s low quality, sh*t, crap, slop, garbage, choose your pejorative.

The thing about this criticism is that it is objectively true. No one watches, listens to or plays most of the stuff on YouTube, Spotify or even Steam. On average, it is crap. The other thing about this criticism is that it is irrelevant. In a power law, there is no arithmetic average, and in a power law popularity distribution, the average is inconsequential. What matters is the head of the curve, the most popular stuff. That’s what’s competing for consumers’ time. And the “quality” of the head will likely keep getting better relative to corporate-produced content.

Most creator content is not good, but most isn’t what matters; the best, most popular stuff is what matters.

GenAI Production Values Will Keep Improving

I won’t belabor this, because anyone who has been paying attention knows that the output quality of GenAI text, image, audio and video models—whether Claude 3.5 Sonnet, Midjourney v6 (see below), Suno v.4 or Runway Gen-3—is advancing at a dizzying pace.

Source: Henrique Centieiro and Bell Lee.

The Consumer Definition of Quality is Shifting Toward Creator Content

Another reason the quality distinction will blur is because the definition of quality itself is changing.

Corporate media will have the edge in production values for some time, but production values are becoming less important to consumers.

I often write about the shifting consumer definition of quality, such as here. In a nutshell, the idea is that quality is not a stated opinion or judgment, but is revealed preference: people’s choices implicitly indicate that what they choose is higher quality to them than what they don’t. These choices—and therefore the definition of quality—change over time.

One of the biggest challenges for anyone who has been in a field for a long time is that they tend to get anchored to a relatively fixed definition of quality. Consumers’ definitions, however, are fluid. When new entrants enter markets with new features, they often change consumers’ definition of quality in the process. This is especially true of younger consumers, whose definitions of quality aren’t as established.

The creator economy is introducing new attributes that are changing the consumer definition of quality, like authenticity, relatability, intimacy, social relevance (whether to a small community or to broad cultural fluency), digestibility, indie, underground, niche, low friction, etc.

By inference, that’s happening today across media. The creator economy is introducing new attributes that consumers clearly value, like authenticity, relatability, intimacy, social relevance (whether to a small community or to broad cultural fluency), digestibility, indie, underground, niche, low friction, etc. Every time that someone slumps on the coach and picks up their phone to scroll through Reels, rather than watch Netflix on the TV that sits mere feet away, they are implicitly indicating that Reels is “higher quality” than Netflix, at least in that context.

It’s also backed up by research. In a recent study of 12,000 video viewers by YouTube, 90% of respondents said that quality is determined by both technical (i.e., production value) and emotive markers. These emotive markers include “really means something to me personally,” “is relevant to my interests and preferences,” and “is authentic and relatable.”

Very little of creator content needs to be good for it to yield a lot of good content.

Internet Scale

The vast scale of creator content means that very little of it has to be good for it to yield a lot of good content.

Refer back to Figure 10. Hollywood produced about 15,000 hours of new TV and film last year, compared to close to 300 million hours uploaded to YouTube. That means that if only 0.01% of YouTube content is considered competitive with Hollywood content (not comparable, but competitive for time), it would yield 30,000 hours of competitive content, 2x Hollywood’s annual output.

Some Established Talent Will Defect

One of the four “tectonic” trends in media that I write about is disintermediation: technology is making it easier for creators (and creatives, who are all latent creators) to produce, market, distribute and monetize content by themselves, increasing their bargaining power over intermediaries or enabling them to circumvent them altogether.

Over the next decade, more established talent may start to question the relative benefit of sticking with traditional intermediaries. As economic pressure grows on traditional media companies, they will become more risk averse, stingier and generally less fun to work with. At the same time, it will become increasingly viable and potentially more lucrative for talent to go it alone.

This has already occurred in journalism. Top journalists like Matt Taibbi, Bari Weiss, Glenn Greenwald, Matt Yglesias, Casey Newton and others have left established news outlets for Substack to gain freedom and, apparently, generally make more money. Over time, this may become more common in other media too.

4. Rising Distrust of Centralized Institutions and Demand for Authenticity Structurally Favors Creators

In the U.S., and probably most of the west, trust in centralized institutions has been falling for decades. Trust in government is at all-time lows (Figure 11) and, more to the point, so is trust in mass media (Figure 12).

Figure 11. Trust in Government Has Been Falling for Decades…

Source: Sources: Pew Research Center, National Election Studies, Gallup, ABC/Washington Post, CBS/New York Times, and CNN surveys.

Figure 12. …As Has Trust in Mass Media

Source: Gallup.

Trust and authenticity are complicated issues in the creator economy. Many creators aren’t considered authentic. Those who are can quickly lose trust and audience if they are perceived as too commercial.

Structurally, the direct relationship between creators and consumers creates more natural conditions for perceived authenticity.

But the creator-consumer relationship is parasocial: because it is often unvarnished, unmediated and “un-institutional,” fans feel like they personally know the creator. Structurally, this unmediated relationship creates more natural conditions for perceived authenticity. Also, when a creator earns trust, it tends to be more personal and resilient compared to institutional trust.

5. The Demise of Monoculture

Many have lamented the end of “monoculture,” big shared cultural experiences. As I explained in Power Laws in Culture, cultural touchstones still exist—Taylor Swift, the Super Bowl, Barbenheimer, GTA 6—but they are fewer and further between. Underscoring the degree of atomization today, according to YouTube’s recent Culture and Trends Report, half of GenZ respondents say that they belong to a fandom that “no one they know personally is a part of.”

We might be nostalgic for monoculture, but recall that mass media is only 100 years old. It might not be the natural state.

Most of the people reading this likely grew up with monoculture—I distinctly remember the finale of M*A*S*H*, when over 100 million people tuned in—but keep in mind that mass media is only 100 years old. We might be nostalgic for monoculture, but perhaps it is not our natural state, at least not most of the time.

Attention has atomized not only because there is much more choice, but, by inference, people don’t actually want a monoculture.

Part of the reason that attention has fragmented is the massive increase in choice. (Again, see Figure 10.) But the mere availability of vastly more stuff is an insufficient reason. It must also be the case that people are choosing to spend their time with a wider variety of content choices, or what we could call microcultures.

Put differently, whether you think the decline of monoculture is good or bad, it’s happening because people prefer the alternative. We can infer a bunch of reasons why. People have varied taste and they no longer need settle for homogenous content; in a world of near infinite choice, what you read/watch/listen to becomes a more powerful way to signal identity and individuality; and it’s more fulfilling to be part of a smaller, more passionate, more engaged community, etc.

But the reasons don’t really matter. When offered more choices, consumers are taking them. The implication is that as the relative volume of creator/independent content choices grow, consumer attention will fracture even more. Economically, corporate media is only viable if it programs to a wide audience. Further atomization into microcultures definitionally means more share shift away from corporate media.

6. Demographics Foretell a Perpetual Shift Toward Creators

If you ever spend time around GenZ, or even occasionally see them slouched over a phone at a neighboring table at a restaurant, it seems obvious that younger consumers spend more of their time with creator content than do other age cohorts. It is probably not worth litigating the point, but here are a few graphs for the heck of it:

Figure 13. Over 1/3 of GenZ is on Social Media >2 Hours Per Day

(1) Question: How much time, on average, do you spend on social media (not including messaging apps) per day. Source: McKinsey Health Institute survey, April 2023.

Figure 14. Almost 3/4 of Adults 18-29 Follow Creators

Source: Pew Research Center survey of U.S. Adults, July 5-17, 2022.

Demographics are destiny.

As time marches on, these younger demos will make up a larger portion of the consumer base and today’s older demos will, well, not. If younger demos maintain their disproportionate usage of creator content as they age, it will be a perma-tailwind for the creator economy.

7. The Monetization Gap Should Narrow

The creator media economy’s share of M&E revenue lags its share of time spent, although it’s hard to tell how much.

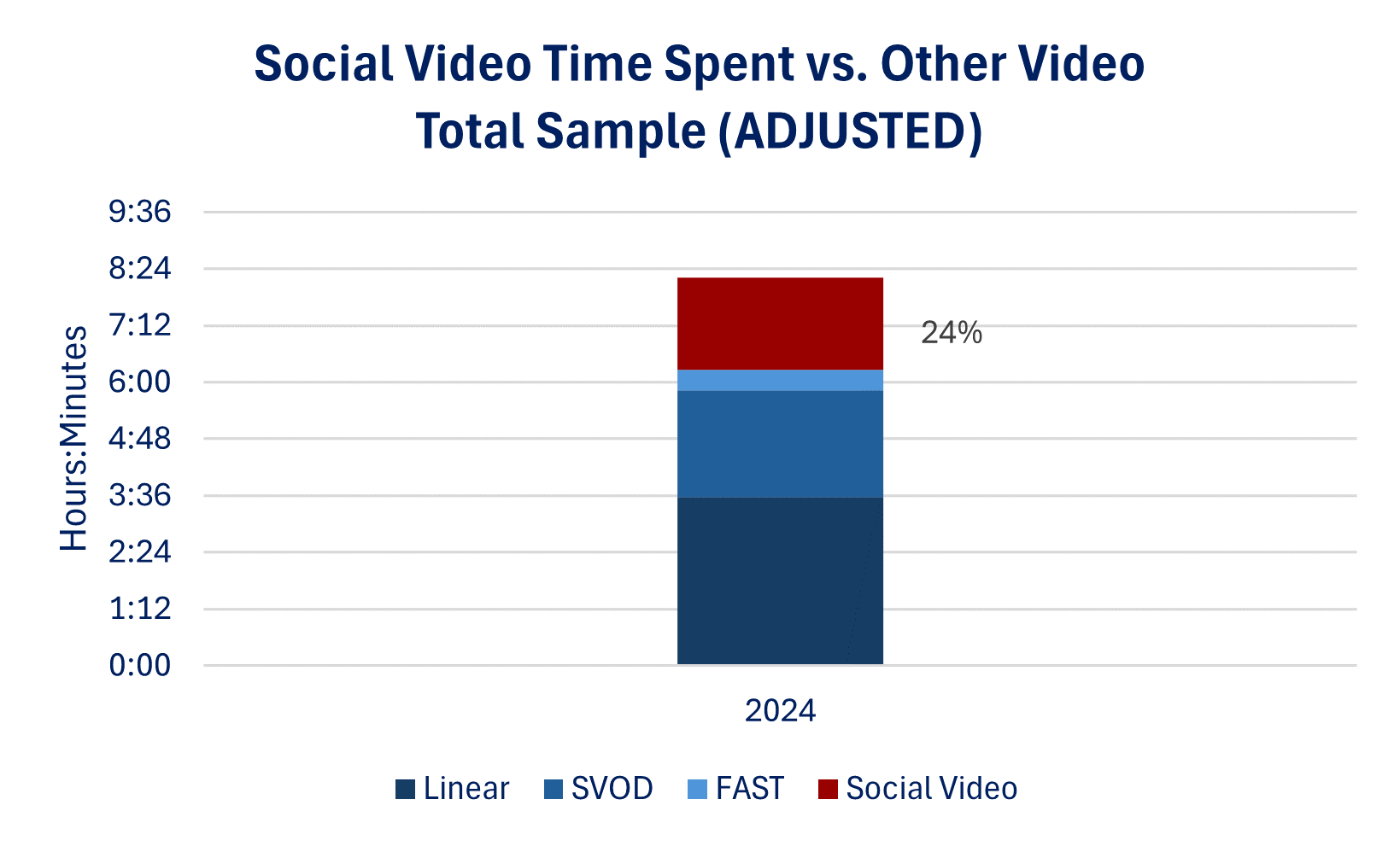

Above, I estimated that the total creator media economy is about 10% of M&E revenue globally. That’s probably substantially lower than its share of time. As shown in Figure 15, I estimate that social video represents about 1/4 of all time spent with video in the U.S. (For more detail on how I derived this, see here.) And, as shown in Figure 16, according to Spotify, about 1/4 of all streams are now derived from artists not represented by the majors or Merlin. These are probably decent proxies for the share of total media time spent with creator/independent content.

Figure 15. Social Video is ~1/4 of Total Video Consumption

Source: Maverix Insights MIDG data, Nielsen, Author analysis.

Figure 16. Similarly, About 1/4 of Spotify Streams are Attributable to Creators/Independents

Source: Spotify.

Over time, the gap between creator economy share of money and share of time should narrow.

Over time, this monetization gap should narrow, even if it won’t likely close completely.

“Money follows eyeballs, with a lag.” This is an old expression in the marketing business. It lags because new outlets necessitate new formats and creative; measurement and attribution; planning and budgeting processes and cycles, etc. Plus, a lot of ad allocations are still driven by relationships. Most advertisers don’t do zero-based budgeting, starting from scratch each year, but base their current year media plans in part on last year’s. But, as new practices, processes and systems fall into place, budgets eventually shift.

There is an ongoing mix shift to digital-native enterprises. Just as younger consumers tend to spend more of their time and money on creator content, younger businesses do too. There is a kind of “demographic effect” in the enterprise. These digital-native businesses allocate more of the their budgets to the creator economy, so as they inevitably become a larger proportion of the global economy, this represents another tailwind.

Creator monetization models should continue to mature. Current creator monetization models are still relatively young. Subscription and patronage platforms like Patreon and Substack only emerged in the last decade (Patreon launched in 2013, Substack in 2017). Primarily ad-supported platforms, like Instagram, YouTube and X/Twitter, have only recently enabled creators to offer subscriptions. Just as traditional media took decades to optimize its business models (cable bundles, retransmission fees, windowing strategies), the creator economy should see similar refinement and “hardening” of business models over time.

“Less Than” or Not, It’s Where the Growth Is

I used the words “inevitable and relentless” in the title of this piece because there are so many tailwinds at the back of creator media, it’s hard to see why the trend reverses. It’s really just a question of how fast it proceeds.

For creators, the future is likely a mixed bag. It’s great to have the wind at your back and monetization tools and models should continue to improve. The offset is that competition is near infinite, power laws are merciless, and the ranks of losers will outnumber the winners by many orders of magnitude.

Creatives will face a perpetual question of when and whether it is better to disintermediate traditional intermediaries and go direct. For many creatives, they have not historically thought like owners, but ownership of their output—and creative control—will be an increasingly viable option.

For traditional media companies, the growth of creator media may be unsettling, but it’s time to move into the acceptance phase of the five stages of grief. There are only two choices: figure out how to participate in the creator economy or accept a perpetually shrinking business.

In a nod to Samir’s distinction between creative and creator, note that I’ve used the term “creative” in Figures 1 and 2 and “creator” in Figure 3.

Note also that I have avoided using the word “professional” in these definitions, because plenty of creators earn money and are, therefore, professionals.

Through the first nine months of 2024, Meta and YouTube advertising have grown by 22% and 15%, respectively, good proxies for overall creator media economy growth.

Great post. I probably take slight issue with the characterisation that “we” the establishment are a bit sniffy toward the creator community. I think we rather look toward it with envy. The envy born from the creative freedom and lack of barriers to entry. When the internet was conceived by Tim his vision was for democratisation of content IP writing etc now the internet is owned by big players, manipulation by agents on all sides is rife and algorithms have become the new gate keepers. And the creator community is becoming owned and controlled in the same way. So the platforms used by the creators are used just as much by the establishment a video clip from one of my shows featuring the sacred Rihanna is still up there in terms of views. Every production has a digital strategy. So do I see the two entities as warring factions, no and I certainly don’t treat it or any new creators with any lack of respect. I look to them for inspiration!

This is brilliant, Doug. Enjoyed the post-Christmas reading.

One platform to watch in 2025 is Bleacher Report, especially regarding your last paragraph. B/R (a subsidiary of WBD/TNT Sports) has made it a mission to embrace the creator economy while remaining under the traditional corporate media umbrella.

The platform always invited users to engage with, and sometimes, create their content, but mainly via the written form — (this was the original mission of B/R before it got scooped up by Turner when the blogosphere was still dominating as the "new kid on the media block"). Now they have launched their "creator program," allowing users to "go live" on video in their product as a reaction to certain games and other tentpole events in the sports world.

While leaning toward the slightly vague branding as "Twitch but for Sports" B/R still hasn't reached the level of Amazon's platform as it still has creators go through a thorough vetting process before allowing them the tools to go live, strongly gatekeeping who and who can't use their live video tools in their app. I believe the vetting process /before/ going live is probably constrained due to staffing on the content moderation side. (Maybe AI can help alleviate this problem down the road...?).

Although I can't go into too much detail, I do know that B/R is going to lean into this strategy even more in 2025 with the launch of an updated product. This paired with B/R's partnership with House of Highlights and its Creator League (https://www.youtube.com/@CreatorLeague) makes it a brand to watch as creator and corporate economies continue their tug-of-war in the back half of this decade.