What Clay Christensen Missed

A Personal Story About How Disruption Happens and Why It’s So Hard to Stop

[Note that this essay was originally published on Medium]

I use the word disruption a lot.

Lately, I’ve been writing about why the last decade in TV and film was defined by the disruption of content distribution and the next decade will be defined by the disruption of content creation (see Forget Peak TV, Here Comes Infinite TV, Power Laws in Culture and Will Radio Save the Video Star?).

In recent years, the word disruption has been thrown around so much that its meaning has become muddled. It is now often used to mean “compete with a different business model and/or technology,” such as “Tesla is disrupting the car market,” “Uber disrupted the taxi business” or “iTunes disrupted the music business.”¹

By disruption, however, I mean the specific definition that the late Clay Christensen first coined when he wrote The Innovator’s Dilemma (1997) and later refined in other books, notably The Innovator’s Solution (2013), and a Harvard Business Review article, What is Disruptive Innovation? (2015).

I come back to this framework time and again because I think it is one of the most powerful descriptive and, increasingly, predictive models for thinking about how big established industries, with massive resources, are upended by tiny bootstrapped upstarts.

But reading about it can seem abstract and academic. It isn’t academic to me. The most formative event in my professional life was watching Time Warner, and the broader TV industry, get disrupted over about a decade. In this essay, I’ll describe my own experience with disruption and one thing that Christensen missed: why it is so hard to stop even when you see it coming from far away.

Clay Christensen’s Disruption

There are plenty of great places to read about Christensen’s definition, including the excellent and accessible (if dense) source material. But to make sure we’re on the same page, here’s my synopsis from The Four Horsemen of the TV Apocalypse, which encompasses both what Christensen referred to as “low-end” and “new-market” disruption:

A new entrant targets a market, usually one that overserves a significant portion of its customers (and/or prices out a lot of non-customers) with a product that overshoots their needs and costs too much. Enabled by a new technology and equipped with a new business model (which are individually or collectively a “disruptive innovation”), it offers an inferior product at a lower cost.

The incumbents dismiss the threat or compete the only way they know how — by making their product even better along traditional performance measure(s) (referred to as a “sustaining innovation”) — and cede the low end of the market.

The upstart’s product continues to improve along the traditional measures of performance, picking off a progressively larger percentage of the incumbents’ customer base or attracting new, previously unserved customers.

The upstart also often introduces a new set of features, which, if successful, changes consumers’ definition of quality (i.e., introduces new measures of performance) and the bases of competition.

After watching their core business erode, the incumbents finally throw in the towel and try to mimic the insurgent’s business model, if they can. Usually, they are ill-suited to do so and it’s too late anyway.

In a nutshell: someone shows up with a cheap, crappy product (or, as Chris Dixon would say, something that “looks like a toy”), the incumbents ignore it and then it keeps getting better and eats their lunch.

What’s implied here is that the incumbents don’t see this all coming. They are fat and arrogant and then the upstart’s success sneaks up on them. That’s not always how it works.

The Innovator’s Dilemma implied that companies get disrupted because they don’t see it coming, but that’s often not how it works.

Time Warner, Netflix and Why Disruption is So Hard to Stop

In 2008, I was running investor relations for Time Warner, which at the time comprised AOL, HBO, Time, Inc., Time Warner Cable, Turner and Warner Bros. Netflix was a scrappy little company with a $2 billion market cap and an aspirational name that mostly sent DVDs in the mail. (“Mailvids” doesn’t have the same ring to it.)

A year earlier, it had begun offering its highest tier subscribers the ability to also stream some old movies online, at no extra charge. At the time, no one thought much of it, even within Netflix. According to The New York Times:

[CEO Reed] Hastings does not believe that electronic distribution, be it through downloads or streaming services, is ready for prime time. “The market is microscopic,” Mr. Hastings said. “DVD is going to be a very big market for a very long time.”

Within Time Warner, we didn’t pay too much attention to the streaming service. We mostly talked about how Netflix’s subscription DVD-by-mail business was undermining our DVD sales.

And then, within a few-week period at the end of 2008, something changed. Netflix licensed TV series rights from both Disney (a few Disney Channel shows, including its biggest hit, Hannah Montana) and CBS (hit scripted series, like CSI). More important, it struck a deal with Starz to license the entire Starz library (~2,500 movies), including Disney and Sony pay 1 window movie rights — i.e., the rights to stream movies like Ratatouille six–nine months after they were in theaters. Even though Starz was generating around $300 million annually from cable and satellite affiliate fees for its premium network, the deal called for Netflix to pay $25–30 million per year for the same content, delivered in a better experience (because it was all on-demand). Years later, subsequent Starz CEO Chris Albrecht would call the deal “terrible.” It wasn’t terrible just for Starz.

In 2008, suddenly, it was possible to foresee the big media companies empowering Netflix by licensing it successively better content with successively shorter windows.

Suddenly, it was possible to foresee the big media companies empowering Netflix by licensing it successively better content with successively shorter windows. Our competitors were acting like licensing to Netflix was found money — which, at the beginning, it was. Wall Street was inconsistent about it: on the one hand, it was concerned about the long-term implications; on the other, it applauded the near-term earnings boost. Within Time Warner, many of us believed it would eventually come home to roost and undermine the linear TV business. Netflix would become the foremost topic of internal debate and concern until the day I left, more than a decade later.

Internal Dissension

In late 2008 or early 2009, Kevin Tsujihara, who was then head of Warner Bros. Home Entertainment, and Thomas Gewecke, head of Warner Bros. Digital Distribution, lobbied our CEO Jeff Bewkes to acquire Netflix. As mentioned, Netflix’s market cap at the time was only several billion dollars.

Jeff asked Kevin to discuss the idea with several HBO executives, who were also tracking Netflix carefully. I wasn’t involved with those discussions and only heard about the outcome afterwards. The HBO contingent argued that Netflix would never turn a profit and was overvalued and effectively killed the idea.

That’s not to say that we would’ve prevailed in trying to buy it and Netflix would almost certainly have not succeeded the way it has were it instead a division of Time Warner. Had we acquired it — and, most likely, inadvertently smothered it — perhaps some other new entrant would’ve stepped into the breach and created a Netflix-like juggernaut. But the idea makes for an interesting alternate history.

Time Warner kicked around the idea of buying Netflix as early as late 2008/early 2009.

External Pressures

Other than some deep library movies and a few series, our filmed entertainment division, Warner Bros., was one of the last holdouts in signing a big licensing deal with Netflix. In late 2010, Jeff gave a speech at a UBS investor conference in which he laid out our intention to license current shows to Netflix in the same window as broadcast and cable TV syndication, namely four years after debut for comedies and procedural dramas, as well as older content that couldn’t otherwise be monetized.

We arrived at this structure deliberately. Prior to the conference, I organized several meetings with the top executives from HBO, Turner, Warner Bros. and Time Warner corporate so we could hash it out and agree on a framework that worked for all our business units.

Netflix was understandably pushing for better content and shorter windows. Our competitors complied. Earlier that year, NBC agreed to license off net dramas and comedies as well as Saturday Night Live episodes one day after airing. Disney also struck a comprehensive deal to provide Netflix with its most successful scripted shows and more of its kids programming, including some content only 15 days post broadcast.

With little high-margin SVOD licensing revenue, our earnings and stock started to suffer in comparison with our peers. Eventually, we capitulated.

In 2011, the CW Network, jointly owned by us and CBS, struck a $1 billion, eight-year output deal with Netflix. Within a few years, we were the largest licensor to Netflix in the industry.

After initially holding out, we eventually became the largest licensor to Netflix in the industry.

A Complex Ecosystem

We also tried hard to improve the value proposition of traditional pay TV.

In 2009, Jeff and Comcast CEO Brian Roberts jointly announced “TV Everywhere,” an effort to enable pay TV subscribers to access on demand content at no extra charge. The content would be available on networks’ websites (and, eventually, mobile and connected TV apps) as well as distributors’ on demand services. Technologically, for consumers to access these websites and apps required that their distributor (i.e., cable, satellite or telco) communicate with the apps in the background and verify that they are paying subscribers in good standing. That process was called “authentication.”

At the time, I was a big believer that improving the value of pay TV could help stave off the Netflix threat. In hindsight, the idea was DOA. It was what Christensen called a sustaining innovation, designed to make our product better. It didn’t address the fundamental problem: people were paying for too much TV they didn’t watch.

But we tried. We granted TV Everywhere rights to our distributors at no cost to get it to consumers as fast as possible. While our peers liked the TV Everywhere concept, they disagreed with this approach. Most thought they deserved to get paid for granting these extra rights and decided to attempt to extract a surcharge in subsequent affiliate negotiations, which are usually staggered over years. It took a long time before a critical mass of TV Everywhere content was available to consumers.

Once it was widely deployed, usage was disappointing as it became clear that consumers didn’t like jumping around between multiple apps (generally, each network had a separate app). As a solution, we pursued different approaches to create an aggregated TV Everywhere experience, with content from all the major network groups in one place. We decided Hulu would be the best home for all authenticated TV. But that plan required that the distributors go along, because they would need to authenticate their subscribers on Hulu. Some of the largest cable operators refused, because they wanted their own on demand services to be the only aggregation of TV Everywhere content.

Sand in the Gears

Over the subsequent decade I spent at Time Warner, I often found myself trying to convince our executives of the urgency of proactively addressing the impending changes in our business. That is, after all, a big part of the strategy job. Plus, I was hardly the only one and I’m sure my foresight at the time seems a lot better in hindsight now. But I earned a reputation for it.

Kevin took to calling me Dr. Doom whenever I’d see him. “Better to be a Marvel character than a DC character, I guess,” was my pat response. When I left the company, I was given a mug that had printed on it “CFO — Chief Fear Officer.” I preferred CUE, Chief Urgency Officer, but whatever.

Many of our senior executives needed no convincing, like Jeff and my boss, Time Warner CFO (and later Turner CEO) John Martin. Others did, either because they couldn’t get their head around how fast things were shifting or it was not in their self-interest to do so. The former were usually benign enough. The latter were often experts at throwing sand in the gears.

Preventing change is a lot easier than effectuating it.

In big companies, preventing change is a lot easier than effectuating it. Once the force of an organization is moving in one direction — the internal processes, the culture, the “narrative,” the incentive system — it is very difficult to shift course. This gives an outsize power to those who have a vested interest in the status quo. It is corporate judo; they are able to use the momentum of the enterprise to their advantage. It takes a lot of “yesses” to effect change. Often, one well-placed “no” can stymie it.

It takes a lot of “yesses” to effect change, but one well-placed “no” can stymie it.

I name no names to protect both the innocent and the guilty. But there are no villains in this story, just people acting in their own interests, as most people do.

Ultimately, Jeff understood the threats better than I did. For years, I (and many others) advocated for us to aggressively launch a Time Warner-wide SVOD product, branded HBO, even if it pressured earnings near term. (This was a variant of Disney’s subsequent big pivot into streaming and what would eventually become HBO Max under AT&T’s ownership). Instead, Jeff chose to sell the company to AT&T. That decision looks more prescient by the day.

Jeff’s decision to sell Time Warner looks more prescient by the day.

What Christensen Missed

The subtitle of The Innovator’s Dilemma, first published in 1997, is When New Technologies Cause Great Firms to Fail. Christensen’s initial thesis was that “great firms fail” when faced with disruption “by doing everything right,” namely “listening to their best customers” and making their products even better. He updated his thinking in 2015, adding another root cause:

First, researchers realized that a company’s propensity for strategic change is profoundly affected by the interests of customers who provide the resources the firm needs to survive. In other words, incumbents (sensibly) listen to their existing customers and concentrate on sustaining innovations as a result. Researchers then arrived at a second insight: Incumbents’ focus on their existing customers becomes institutionalized in internal processes that make it difficult for even senior managers to shift investment to disruptive innovations.

Both of these may be true, but it is an incomplete explanation.

Firms get disrupted because they have many stakeholders with misaligned interests, not because they don’t see it coming or know what’s at stake.

Often, firms get disrupted not because they don’t understand the disruption process, see it coming or know what’s at stake. They don’t even get disrupted because of the difficulty of changing internal processes. They get disrupted because companies operate in complex ecosystems of stakeholders with misaligned interests: employees (including well-paid, powerful executives), unions, vendors, distributors, “complementors,” board members, shareholders, etc. This is why disruption can be virtually impossible to head off even when you see it coming from far away.

It Feels Like 2008 Again

As mentioned at the beginning, lately I’ve been writing about the risk that, just as video content distribution was disrupted 15 years ago, content creation is on a path to be disrupted next.

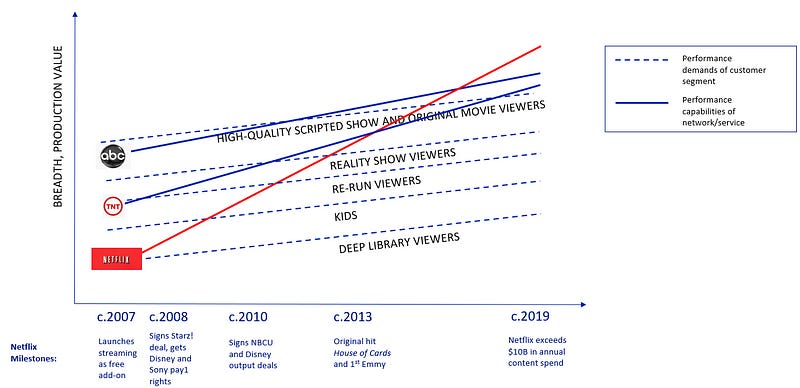

Visually, this looks like the graphs below. Figure 1 shows the disruption of content distribution. Netflix starting with a “crappy” product and successively moved up the performance curve, picking off more of the incumbents’ customers along the way. As depicted in the graph, today Netflix is not only a better offering than broadcast or cable, it is arguably overserving customers with too much good content.

Figure 2 illustrates the potential disruption of content creation over the next decade, with YouTube acting as proxy for independent or creator content. Today, YouTube already competes for some customers’ time and attention, like kids and viewers of some unscripted content. But broadcast and cable budgets are getting cut, which will likely result in declining performance. At the same time, virtual production and AI promise to democratize high-quality production tools, which will increasingly blur the quality distinction between professionally-produced narrative fiction and independent content — and pour gas on the fire.

Figure 1. The Disruption of Content Distribution Over the Past Decade or So

Figure 2. The Disruption of Content Creation Over the Next One

Source: Author

I’ve seen a fair number of tweets recently touting the latest generative AI tool and saying that “Hollywood is over” or “dead.” I don’t think Hollywood is dead by any means. But the disruption of content creation could have an even larger effect on the industry than the disruption of distribution did because it is more central to what it does. And having had a front row seat to the disruption of content distribution over the last decade, I think that it too will be very hard to stop.

¹ For what it’s worth, none of these examples are disruptive according to Christensen’s definition.